The Crisis in Auto Loans. 2007 was Sub-Prime Mortgage. Is 2026 Auto?

Published: April 22, 2026

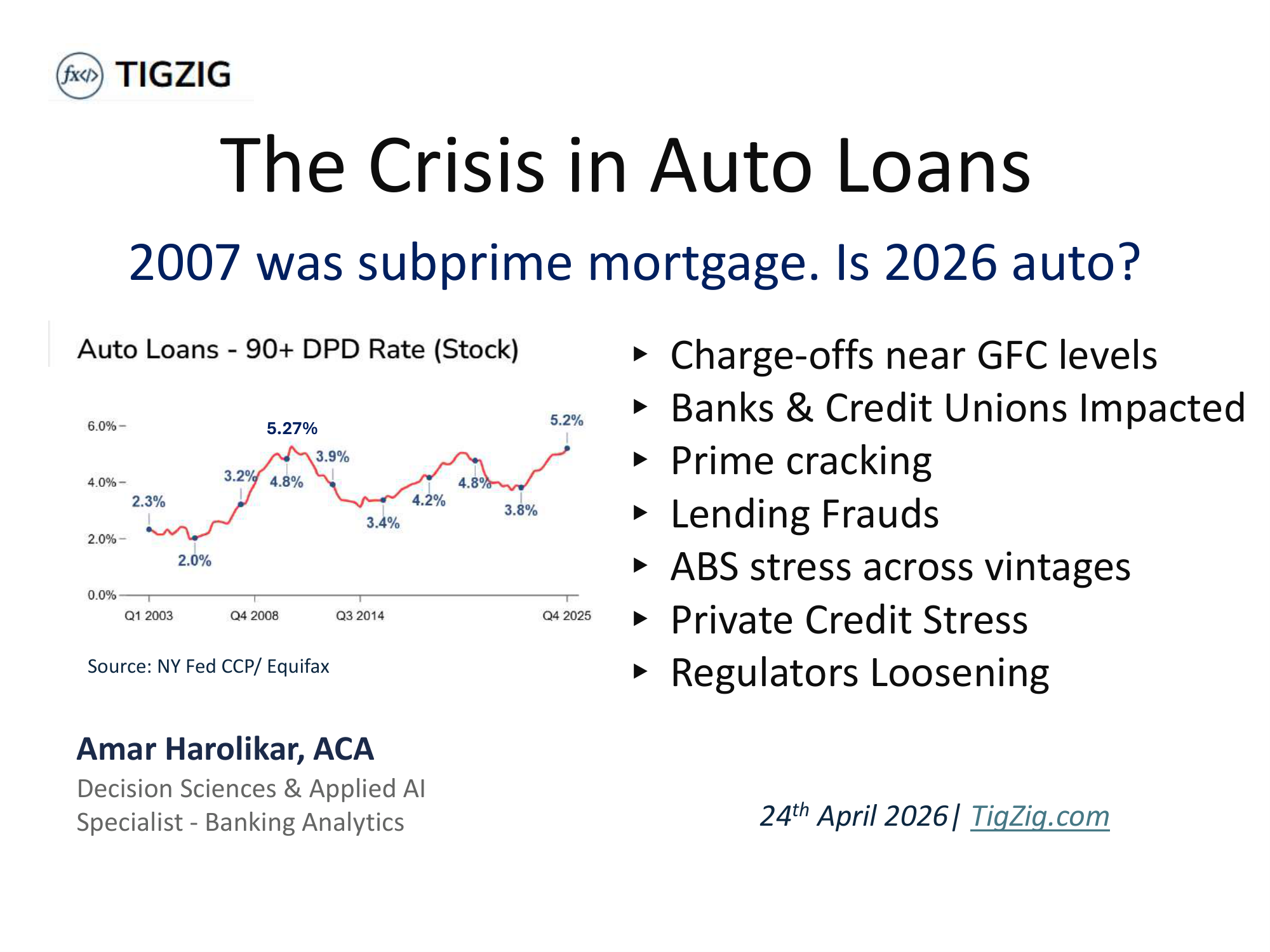

NY Fed Auto 90+DPD at 5.21% vs 5.27% at GFC peak. 2007 was subprime mortgage. 2026 is shaping up to be auto. Losses at Banks and Credit Unions at GFC levels - on cleaner, prime-weighted post-GFC book. Same rate on a cleaner book = worse underlying stress.

When prime credit unions crack, the stress is mainstream, not tail.

Now add frauds surfacing in private credit, undisclosed insurer exposure, rising unemployment, oil shock, AI displacement of labor, and regulators pulling back exactly when risk is building...you have the makings of a systemic event.

Here's what I found running FDIC SDI data for the last 100 quarters, NY Fed CCP, NCUA Credit Union data, S&P Global ABS Tracker, and FFIEC Call Reports for all 629 NDFI-lending banks:

- Bank auto NCO at 2X the 2011 baseline

- Credit union NCO at 0.95% (Q4'25) - record high in the series

- NY Fed 90+ DPD at 5.21% (Q4'25) vs 5.27% at 2010 GFC peak

- S&P ABS: subprime NCO at ~10%, prime cracking at ~6% (Feb'26)

- Tricolor fraud: $800M phantom collateral

- First Brands fraud: $2.3B off-book receivables vanished

$1.67T direct exposure. $350B more in ABS. Plus undisclosed exposure through bank NDFI books ($1.92T) and PE-owned insurer general accounts.

Auto alone will not break the system...many stressors hitting together can.

Federal Reserve Bank of Boston called it out in May 2025: "Banks fund private lenders through credit lines and could pose systemic liquidity risk...tail risk may be underappreciated."

Sharing analysis covering delinquencies, bank losses, fraud cases, ABS stress, contagion channels, and regulatory posture. Plus where it fits in the broader macro setup - CAPE at 40x, U-3 drifting 35 months from trough, Hormuz energy shock & AI displacement of labor.

Deck below. Data and interactive drill-down at tremor.tigzig.com

The Crisis in Auto Loans - 2026

Browse the slides or download the PDF

Full Deck Content (Text Format)

Text below was extracted from the source deck. Chart visuals stay in the PDF and as slide images above the post.

US FED Financial Stability ReportMay 2026 Report

Amar Harolikar

Decision Sciences & Applied AI

Read TIGZIG Research here

Most cited potential shocks over next 12-18 months (Fed Survey)4 of Top 6 shocks covered by TIGZIG Research

Read FED FSB Report here

Executive Summary

The auto loan setup in six numbers.

SCALE

$1.67T

Auto loans outstanding. 5.4% of US GDP

DELINQUENCY

5.21%

90+ DPD at GFC peak levels. Prime-book stress without GFC triggers.

BANK LOSSES

1.21%

Bank auto NCO at 2x 2011 baseline. Credit unions at record highs.

FRAUD SURFACING

$3.1B

Tricolor $800M phantom collateral + First Brands $2.3B off-book receivables vanished. Both Sept 2025.

CONTAGION

10 channels

Direct bank losses, ABS spreads, warehouse withdrawals, BDC NAV cuts, redemption gates, insurer writedowns.

REGULATORY STANCE

1 of 5

Only NAIC tightening. Four regulators loosening while risk builds.

Auto alone will not break the system.

Multiple stresses running simultaneously is what does

Auto credit – non-trivial share of GDP, like 2007 subprime mortgage

Sources: NY Fed HHDC Q4 2025 / Equifax | FDIC QBP Q4 2025 | NCUA Q4 2025 | Fed G.20 | Fed H.8 | Fed Z.1 Financial Accounts (insurer GA) | SIFMA US ABS Statistics | BEA GDP | Fed Boston CPP 25-8 (May 2025) | Fed FSR (Oct 2025) | FDIC / NCUA / NY Fed aggregates via Tigzig Tremor platform | Tigzig analysis (residual 'Others' in direct-holders table)

DIRECT

$1.67T

Q4 2025 - NY Fed CCP

INDIRECT EXPOSURE

$350B+

ABS verified. NDFI + insurer channels additional, not publicly sized.

COMBINED vs 2007

~6.5%+ of GDP

vs ~8.3% for 2007 subprime mortgage

DIRECT HOLDERS - who actually has the loans

INDIRECT EXPOSURE - additional channels

Holder | Amount | Share

Banks | $536B | 32%

Credit unions | $484B | 29%

Non-bank finance cos. | $485B | 29%

Others* | ~$165B | 10%

Channel | Total exposure | Auto slice

Auto ABS outstanding | $350B | $350B

Bank lending to NDFIs | $1.92T | Not disclosed

Life insurer GA Unclassified | $1.2T | Not disclosed

P&C insurer other equity | $351B | Not disclosed

*Others = BHPH (Buy-Here-Pay-Here) + fintech + subprime specialists. Category-level breakdown is not publicly measured; figure is a residual to the NY Fed panel total.

Auto-specific slice of NDFI lending and insurer exposure is not publicly disclosed. For reference: auto loans are ~4% of total FDIC bank loans and ~27% of consumer loans. The Federal Reserve Bank of Boston (May 2025) and Fed FSR (Oct 2025) have flagged the NDFI disclosure gap as a systemic concern.

Auto loans carry different risks than mortgages. Collateral depreciates. Recovery is fast but lossy. Stress now visible in both prime and subprime.

GDP denominators: US nominal GDP ~$30.8T (2025, BEA) | 2007 US GDP ~$14.5T. 2007 subprime mortgage ~$1.2T = 8.3% of GDP.

The auto loan ecosystem - banks, captives, private credit and insurers all carry the risk

BORROWER

LENDING CHANNELS

FUNDING SOURCES

CAPITAL MARKETS

US auto loan borrowers

~$1.67T outstanding (Q4 2025, NY Fed/Equifax) - ~15% subprime (FICO <620)

Banks (direct)

$536B | 32% Ally, Chase, Cap One

Credit unions

$484B | 29% NCUA-regulated

Captive finance

$485B | 29% Toyota, GM, Ford, Stellantis

Others*

~$165B | 10%

Deposits

Banks and credit unions fund loans from customer deposits

Parent / corporate debt

Captives issue unsecured bonds, CP, OEM credit lines

Auto ABS market

~$350B outstanding | ~$127B '25 issuance

Held by banks, MMFs, asset mgrs

Bank NDFI book

~$1.92T (Fed H.8) | 34% of large-bank C&I

Includes warehouse lines to non-bank auto lenders

Sources: NY Fed HHDC Q4 2025 / Equifax | FDIC QBP Q4 2025 | NCUA Q4 2025 | Fed G.20 Finance Companies | Fed H.8 NDFI lending | NAIC Capital Markets Bureau ABS Report (YE 2023) | Fed Z.1 Financial Accounts | SIFMA US ABS Statistics | FDIC / NCUA aggregates via Tigzig Tremor platform | Tigzig analysis (residual 'Others' and channel-to-funding mapping)

Insurer General Accounts

$33B auto ABS disclosed (NAIC YE'23)

Add'l unclassified GA at PE-owned life cos - not sized

- BHPH dealers, fintech, subprime specialists - residual to NY Fed total

Private Credit + Insurer Whole-loan Buyers

PE-owned life cos and PC funds

Buy whole loans and mezz ABS tranches

Capital recycled to fund new originations

Delinquencies & losses at GFC levels

Source: NY Fed Consumer Credit Panel / Equifax | data via Tigzig Tremor platform

Auto 90+ DPD at 5.21% (Q4 2025) vs 5.27% (GFC Peak Q4 2010) GFC levels without GFC triggers. In 2010, 5.27% came after mass unemployment, a housing collapse, and a banking crisis. In 2025, 5.21% arrived with low unemployment and a capitalized banking system. The stress is coming from within the credit system itself - peak collateral prices, rate shock, vintage concentration.

5.27%

About the data

NY Fed Consumer Credit Panel covers all lenders - banks, captives, credit unions, BHPH dealers, and PE-backed subprime specialists.

90+ DPD includes severely derogatory balances: loans already charged off by the originator but still tracked on the consumer's credit file for up to 7 years while collection continues.

ALL LENDERS

Auto losses are already at GFC-peak level. Any new macro shock lands on top of that

BANKS

NCO 1.12% (Q4-2025, annualized) vs 0.64% in Q1-2011

Book composition shift. Post-GFC banks retreated from deep subprime. Same rate on a cleaner, prime-weighted book = worse underlying stress.

Indirect subprime exposure. NDFI warehouse lending to non-bank auto lenders sits outside the charted NCO rate - where Fifth Third, JPM, and Wells took the Tricolor hit (Fed FSR Oct 2025).

Source: FDIC SDI via tremor.tigzig.com, FDIC QBP Q4 2025, S&P Global Auto Loan ABS Tracker (Dec 2025, FY 2025)

Stress has spread from subprime into prime/near-prime. 2022-24 vintages originated at peak loan balances; collateral has come off the peak but loan principal hasn't. S&P data: subprime recoveries fell to 37.74% in 2025, the lowest annual reading since 2007. Subprime annualized losses hit 8.88% and 60-day delinquencies a record 6.18% - losses and loss severity are rising together.

Highest charge-offs since GFC - 2X of 2011

Q4 2020-2021 dip reflects COVID forbearance, stimulus effects, and loan modifications - not underlying credit improvement.

Prime-book stress without a macro shock - the chart understates the risk.

Charge-offs at record highs - on a prime book

0.95% in Q4 2025 - 2.2x the 2013 baseline of 0.43%

Credit unions are not supposed to be here. They run prime, member-based books - so this is typical middle-class stress, not the subprime tail.

Source: NCUA Aggregate Financial Performance Reports (5300 Call Report) for all Federally Insured Credit Unions. Auto = New Vehicle + Used Vehicle loans (excludes leases). Net charge-offs = YTD Charge-Offs minus YTD Recoveries (account codes A550C1/C2, A551C1/C2). Rate shown = quarterly NCO × 4, divided by average of period-end balances (A385, A370) - a quarterly-annualized rate. NCUA's own YTD rate on the same inputs was 0.90% for Q4 2025, smoother because it averages the full year. Quarterly-annualized surfaces the current-quarter peak. All inputs are primary NCUA data. Series starts Q2 2013 when NCUA began separating auto NCO from “All Other Loans.”

NCUA Chairman Harper flagged it directly. “Used vehicle delinquency and net charge-off rates at the highest levels on record” (NCUA Q4 2025 release, March 2026).

CREDIT UNIONS

Q3 2020-2022 dip reflects COVID forbearance, stimulus effects, and member hardship programs - not underlying credit improvement.

When prime credit unions crack, the stress is mainstream - not tail.

Sub 25%

Prime 75%

In ABS - $350B

Total US auto loans outstanding - $1.67T

what it is and where it fits in the market

Sources: NY Fed HHDC Q4 2025 / Equifax | SIFMA US ABS Statistics | S&P Global Auto Loan ABS Tracker | Tigzig analysis (residual "Outside ABS" derivation)

What it is

Lenders pool thousands of auto loans and sell slices ("tranches") to investors as bonds.

Senior tranches get paid first and are rated AAA. Junior tranches absorb the first losses.

Same structural playbook as 2007 mortgage CDOs - different collateral, same layered loss mechanics.

Where it fits in the $1.67T US auto market

Outside ABS: ~$1.32T held directly by banks, credit unions, captives & others

~75% prime / ~25% subprime split

Every ABS deal files monthly investor reports. Rating agencies publish loss curves by vintage. ABS is the cleanest, earliest window into stress across the book

AUTO ABS

The pool is cracking - and so is prime

Stress is bleeding into prime. S&P: 2023 and 2024 prime vintages are the worst in index history.

Issuance at record highs. ~$127B in 2025, 2.5x 2020.

Sources: S&P Global Auto Loan ABS Tracker (Feb 2026) | Fitch Auto ABS Indices (Jan 2026) | SIFMA US ABS Issuance | Tigzig analysis

Subprime charge-offs are running at ~10% and prime is at ~6% in Feb '26 across the S&P Global Auto ABS pool ($176B tracked).

Subprime at its worst on record. Fitch 60+ DPD at 6.9% (Jan '26, highest since 1993).

S&P Global Prime & Subprime Auto ABS 60+ DPD

Amber line (left axis): Prime 60+ DPD. Pink line (right axis): Subprime 60+ DPD.

AUTO ABS

Record issuance while losses are at multi-year highs - the market is behind the curve.

Different decade, same rating failures, new holders

Sources: KBRA Tricolor rating action notes (Sept-Oct 2025) | Exeter EART 2025-5 (ASR/S&P, Nov 2025) | ACAR 2025-4 (KBRA, Oct 2025) | UACT 2025-1 (ASR/S&P, Mar 2025) | Bloomberg / S&P Market Intelligence Tricolor coverage | Tigzig analysis

The 2008 analogue

Rating agencies missed the fraud.

Where it lands now

PE-owned insurers and private credit.

Pricing in more losses

Credit enhancement is rising fast.

Tricolor TAST held AAA three months before Ch. 7. KBRA then cut seniors 19 notches to CC.

Risk moved to PE-owned insurers and private credit. Apollo/Athene, KKR/Global Atlantic, Blackstone/F&G, Carlyle/Fortitude.

New subprime deals price with much larger first-loss cushions below AAA:

Exeter 51% | ACAR 61% | UACT 63%.

AAA protection is only real if the loans are real.

When this cracks, it lands at banks and insurers - not investment banks.

Higher cushions = the market is pricing in more losses.

AUTO ABS

3 cases - the dirt surfacing across credit markets

Sources: DOJ SDNY press release - Tricolor CEO/CFO/COO charged | DOJ SDNY press release - First Brands executives charged | Zions 8-K on SEC EDGAR (Cantor Group charge-off) | JPMorgan Q3 2025 earnings call (Oct 14) | Motley Fool - Dimon cockroach quote transcript (Oct 14, 2025) | First Brands Ch. 11 filings, SDNY / PitchBook coverage | S&P Market Intelligence Tricolor forensic analysis

Case 1 - Tricolor

Pledge it once. Pledge it again.

Case 2 - First Brands

Invoices that never existed.

Subprime auto lender in Dallas. Ch. 7 in September 2025. CEO indicted Dec 2025.

Auto parts roll-up. Ch. 11 in September 2025. Founder and brother indicted Jan 2026.

Case 3 - Cantor Group

Collateral secretly sold to others.

Hit regional banks October 2025. Western Alliance sued Cantor. Zions stock -13% in a day.

$800M phantom collateral. $2.2B pledged vs $1.4B real..

$2.3B off-book receivables vanished.

$50M charge at Zions alone.

Dimon, October 2025, after Tricolor: "When you see one cockroach, there are probably more."

FRAUDS

A shock unlike anything before

Sources: Cox Automotive / Manheim MUVVI (March 2026) | AutoForecast Solutions via Alvarez & Marsal | Cox Automotive July 2021 Inventory | Hertz Ch. 11 (AutoRentalNews) | BLS CPI (Jan 2022 release) | Federal Reserve FOMC | Tigzig analysis

Manheim went vertical in 2021. Prices fell, then bounced.

PRE-2020 BASELINE

~153

Range-bound ~115-155 for 14 years (2006-2019

JAN 2022 PEAK

257.7

+68% in 23 months

MARCH 2026

215.3

35-40% above baseline

Rising 5 months straight

Four forces collided in 2020-2022

1

Chip shortage

~17.7 M units of global production lost. Inventory fell to 25 days of supply (Jul '21).

2

Hertz fire sale

Ch. 11 May '20; forced sale of >182K cars. Industry refleeted at peak in 2021.

3

$814B stimulus

Three rounds of consumer cash. Used-car CPI hit +40.5% YoY in Jan '22.

4

Zero rates

Fed funds at 0-0.25% (Mar '20-Mar '22). New-car APRs at ~3.86%.

USED VEHICLES

The borrower trap: peak collateral & rates, underwater

Sources: Experian State of Auto Finance (Q4 2025 & Q1 2020) | Edmunds Q4 2025 Insights | Cox Automotive / Manheim MUVVI | BLS Motor Vehicle Insurance CPI | AutoRemarketing - Fitch subprime delinquency | Marketplace - 2024 auto repossessions | Tigzig analysis

Step 1 - The loan

Written across peak prices and rising rates.

Step 2 - The collateral

Then the car dropped in value.

Avg new-car loan jumped from $33.7K (Q1 '20) to $43.6K (Q4 '25). New-car APR climbed from 5.6% (Q1 '20) to 6.4%; used-car APR at 11.3%; deep-subprime new-car at 16%.

Manheim fell ~24% peak-to-trough (258 late-2021 to 196 June 2024); now ~16% below peak at 215. Loan amortized slower than the car depreciated.

Step 3 - The squeeze

Stuck on four sides. Only exit is default.

Payment is high. Insurance up 56% since Jan 2020. Wages flat. Selling means writing a check. Refinancing impossible when underwater.

~30% of new-car loans now stretch 6+ years (73-84 months).

29.3% of trade-ins underwater. $7,214 avg neg. equity.

Record subprime delinquency. Repos. at highest since 2009.

USED VEH.

One regulator tightening. Four moving the opposite way.

1

INSURANCE

Tightening

NAIC moves on PE-owned insurer reinsurance.

2

BANKING

Loosening

OCC and FDIC rescinded the 2013 leveraged lending guidance.

3

ENFORCEMENT

Shrinking

SEC enforcement at a decade low.

5

ADMINISTRATION

Opening

Executive Order opens 401(k)s to private credit and PE.

Sources: NAIC Actuarial Guideline 55 (Aug 2025) | OCC Bulletin 2025-44 (Dec 2025) | OCC / Comptroller Gould letter to Sen. Warren (Jan 2026) | CFPB enforcement docket & staff reorganization filings | Paul Weiss SEC Enforcement Review (2025) | SEC investigation of Jefferies / Point Bonita (Nov 2025) | White House Executive Order 14330 (Aug 2025) | DOL guidance rescission (Aug 2025) | DOL Proposed Rule on Designated Investment Alternatives (Mar 2026) | Fed H.8 & Financial Stability Report (Nov 2025) | Tigzig analysis

THE LAW

4

CONSUMER

Shrinking

CFPB has been structurally gutted.

AG 55 adopted Aug '25, first reports due Apr ‘26. Separately, 45% RBC charge on residual tranches (capital). Apollo/Athene cut its CLO book roughly in half (2025)

Comptroller explicit: the goal is to let banks compete with private credit. 6x debt/EBITDA threshold gone. No post-Tricolor consent orders.

313 actions in FY25, down 27% YoY. Nearly 30 cases dismissed since Jan '25. Settlements $808M, down 45%.

Executive Order 14330 (Aug '25) opens 401(k)s to PE, private credit, digital assets.

67 guidance docs withdrawn. 42 enforcement actions dismissed. Staff cut proposed from 1,174 to 556.

Regulators and the Administration are loosening while risk is building

How stress travels through ten channels

Sources: JPMorgan / Fifth Third / Zions / Western Alliance earnings & filings | KBRA Tricolor rating actions | FS KKR & BlackRock TCP 10-Q | Blue Owl OBDC II redemption notice (Feb 2026) | Fed H.8 Bank Lending to NDFIs (Nov 2025) | Fed FEDS Notes (May 2025) Bank Lending to Private Credit | Fed FSR (Oct/Nov 2025) | OFR Annual Report (Nov 2025) | FSOC Annual Report (Dec 2025) | NAIC AG 55 | Raistone / First Brands Ch. 11 coverage | Tigzig analysis

CONTAGION

Direct bank losses

JPM $170M + Fifth Third $178M on Tricolor. Zions $50M on Cantor.

Rating Downgrades

KBRA cut Tricolor TAST seniors 19 notches to CC in one action. Forced selling follows.

ABS spread widening

Subprime BBB spreads widened ~50bps post-Tricolor. Higher cost to issue, lower origination capacity.

Warehouse line withdrawal

Banks tightened warehouse facilities to non-bank auto lenders post-Tricolor. Origination capacity chokes.

BDC mark-to-market

BlackRock TCP marked loans to zero. NAV cuts flow through to LP reporting.

Redemption gates

Blue Owl OBDC II ($1.6B retail fund) halted redemptions Feb '26.

Bank-NDFI linkage

Fed H.8: bank loans to NDFIs ~$1.9T (Feb’26), above Tier 1 at many large banks.

Insurer writedowns

PE-owned life insurers holding mezz ABS face RBC capital hits. AG 55 and 45% residual charge now active.

Counterparty cascade

Raistone Capital (~80% revenue from First Brands) prepping Ch. 7 Jan '26.

Litigation

Class action lawsuits filed against Zions and Jefferies.

Auto is one stress. There are others - converging at the same time.

No single stress breaks the system. Converging stresses do

CONSUMER CREDIT

2.90%

Bank net charge-off rate for consumer. Highest in 15 years; above pre-GFC Q3 2007 (2.47%).

LABOR MARKET

1.8%

U-1 long-term unemployed already above 2007

VALUATIONS

~40x

Shiller CAPE. 2nd time in 155 years. 50% above 2007.

ENERGY

$112+

Geopolitical supply risk elevated. Brent $112+. Normalization takes months.

AI LABOR SHOCK

9X

Duke CFO Survey projects AI-attributed layoffs 9x 2025 baseline

"Banks fund private lenders through credit lines and could pose systemic liquidity risk... tail risk may be underappreciated."

- Federal Reserve Bank of Boston, Current Policy Perspectives 25-8, May 2025

Sources: Anthropic Economic Index - Massenkoff & McCrory (March 2026) | Federal Reserve Bank of Boston, Current Policy Perspectives 25-8 (May 2025) | Fortune CFO Survey (March 2026) | Challenger Gray Report (March 2026) | Tigzig analysis

Data and Methodology

Primary Data Sources

NY Fed Consumer Credit Panel / Equifax

FDIC Call Reports (100 quarters, $13.6T in loans)

NCUA Credit Union 5300 Call Reports

Fed H.8 (Bank Lending to NDFIs)

SEC / EDGAR (BDC filings, 10-K/10-Q)

BLS (unemployment, wages, CPI)

S&P Global, Fitch, KBRA ABS trackers

Tremor - tremor.tigzig.com

Aggregated FDIC, NY Fed data with full drill-down

NCUA Credit Union module (launching soon)

US NDFI exposure module - bank lending to non-banks

Macro signals dashboard and indicators

Credit news tracking

Historical trends, segment views, download options

Charts and aggregates are live on Tremor. Data drawn from primary regulatory sources, supplemented by news coverage and analyst reports.

Sources & Citations

NY Fed Consumer Credit Panel / Equifax (Q3 2025) newyorkfed.org/microeconomics/hhdc

Federal Reserve H.8 (Assets & Liabilities) federalreserve.gov/releases/h8

Federal Reserve Financial Stability Report (Oct 2025) federalreserve.gov/publications/financial-stability-report.htm

Federal Reserve G.19 Consumer Credit federalreserve.gov/releases/g19

Federal Reserve H.15 Selected Interest Rates federalreserve.gov/releases/h15

Fed FEDS Notes - Bank Lending to Private Credit (May 2025) federalreserve.gov/econres/notes

Fed FEDS Notes - consumer delinquency dynamics federalreserve.gov/econres/notes/feds-notes

FDIC Quarterly Banking Profile fdic.gov/analysis/quarterly-banking-profile

SIFMA US ABS Issuance & Outstanding sifma.org/resources/research/us-abs-statistics

IMF Global Financial Stability Report (Oct 2025) imf.org/en/Publications/GFSR

IMF Connect US ABS Monitor (Oct 2025) imfconnect.imf.org

NAIC Capital Markets Bureau ABS Report (YE 2023) content.naic.org

Cox Automotive / Manheim Used Vehicle Value Index coxautoinc.com/insights/manheim-used-vehicle-value-index-march-2026-trends

Cox Automotive - New-vehicle inventory (July 2021) coxautoinc.com/market-insights/new-vehicle-inventories-slumped-to-record-low-as-july-opened

Experian State of Automotive Finance (Q4 2025) experianplc.com

Edmunds Q4 2025 Insights Report edmunds.com/car-news/edmunds-q4-2025-insights-report.html

BLS CPI Used Cars & Trucks (CUUR0000SETA02) bls.gov/news.release/archives/cpi_02102022.htm

BLS Motor Vehicle Insurance CPI factsheet bls.gov/cpi/factsheets/motor-vehicle-insurance.htm

BLS JOLTS - Job Openings & Labor Turnover bls.gov/jlt

EIA - Short-Term Energy Outlook & oil prices eia.gov/outlooks/steo

AutoForecast Solutions - semiconductor shortage alvarezandmarsal.com/insights/production-cuts-increase-chip-shortage-and-supply-chain-issues-persist

Hertz Global Holdings Chapter 11 filing (May 2020) autorentalnews.com/10122085/hertz-settlement-calls-for-disposal-of-182-521-vehicles

Pandemic Oversight - Three Rounds of Stimulus Checks pandemicoversight.gov

NCUA Credit Union Call Report Q4 2025 ncua.gov/analysis/credit-union-corporate-call-report-data

Federal Reserve G.20 - Finance Companies federalreserve.gov/releases/g20/current

Federal Reserve Z.1 Financial Accounts (insurer GA) federalreserve.gov/releases/z1

Tigzig Tremor platform - FDIC / NY Fed / insurance data tremor.tigzig.com

AutoRemarketing - Fitch subprime auto ABS coverage autoremarketing.com/subprime/fitch-continues-dialogue-about-affordability-delinquency

Marketplace - 2024 record auto repossessions marketplace.org/story/2025/11/12/a-record-number-of-americans-are-behind-on-their-auto-loans

GAO-22-106044 - COVID Stimulus Tracking gao.gov/products/gao-22-106044

Federal Reserve Open Market Operations (fed funds history) federalreserve.gov/monetarypolicy/openmarket.htm