Banks Holding the Line.. But the 'Lemons' Sit Off the Chart. In Private Credit, Credit Unions, and Non-Bank Consumer Lenders.

Published: May 29, 2026

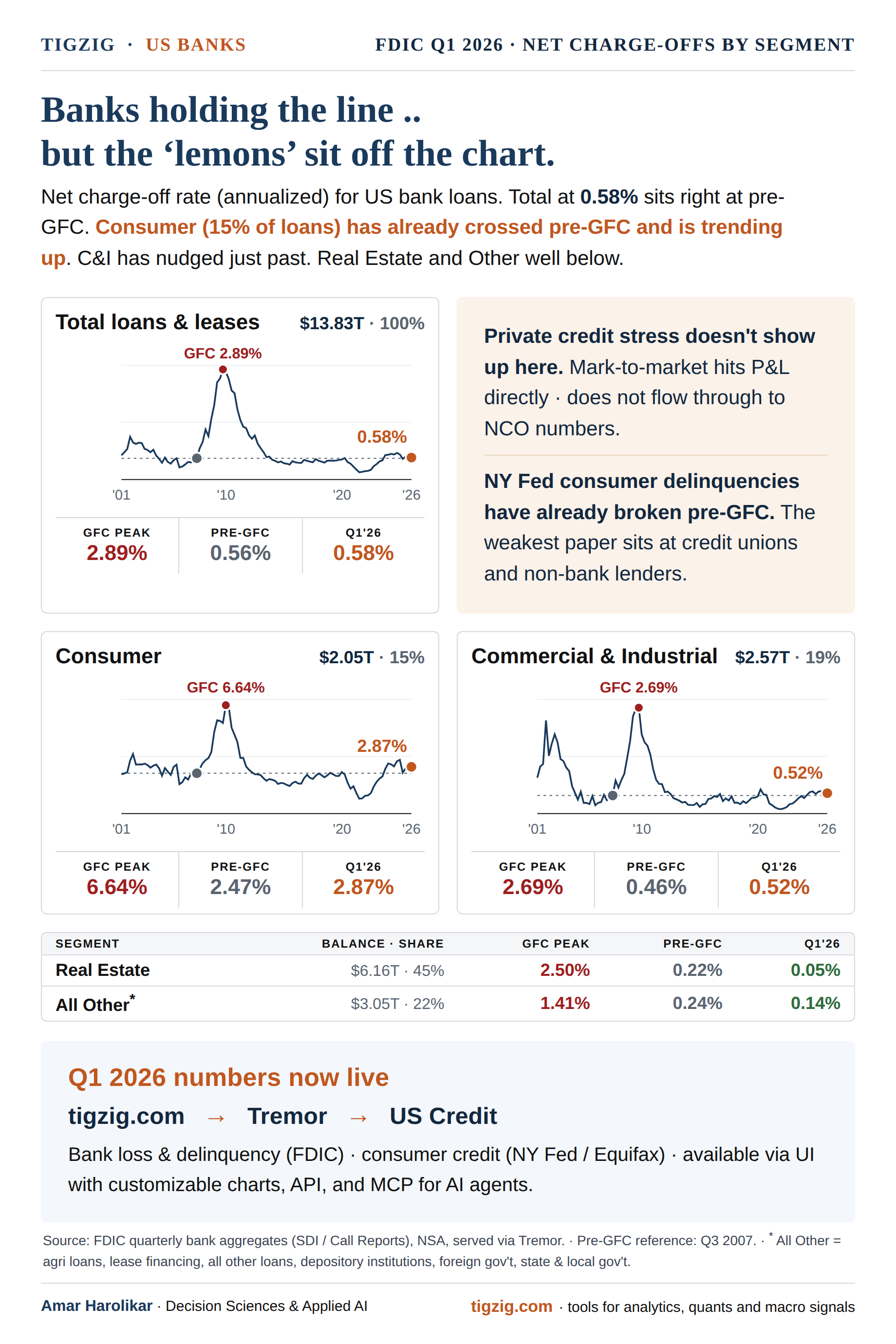

Banks holding the line... but the 'lemons' sit off the chart. In private credit, credit unions and non-bank consumer lenders.

The chart shows US bank NCO right at pre-GFC. Real Estate, the biggest chunk, is holding well. Consumer and C&I inching up but nothing terrible.

The stress on the financial system is in two places the bank NCO doesn't show.

1/ Private credit.

Marked to market, hits P&L directly. Doesn't flow through to NCO. DOJ probing valuation marks at a BlackRock private credit fund. FSB warning on data gaps, valuation and opacity. Bank of England calling it a 'market for lemons'. ECB flagging it as a spillover risk to the euro area. Bank loans to non-bank lenders crossed ~$1.6T (FFIEC) - about a fourth is private credit. Insurers in deep too.

2/ Credit unions and consumer outside the bank.

Credit union consumer NCO at 1.82%, nearly 2x pre-crisis. Cards at 5.11%, past the 4.68% GFC peak. NCUA itself flagging cards past GFC peak, used vehicle loans at highest on record. Non-banks carrying the weakest paper.

Detailed analysis at tigzig.com/analysis.