US Bank Exposure to Non-Bank Lenders - Now in an Interactive Analytics Tool

Published: April 4, 2026

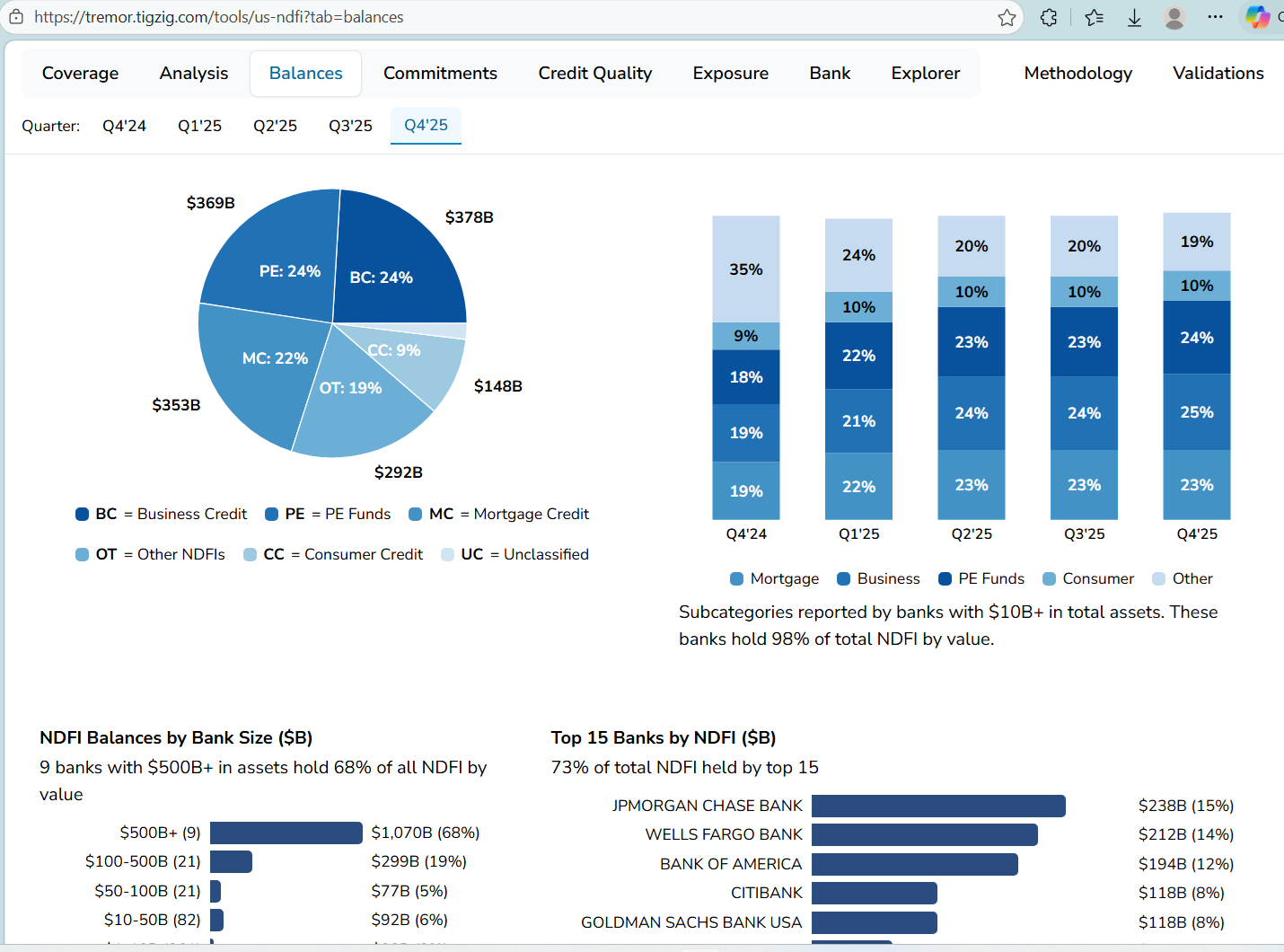

Run your own cuts. 629 banks, $1.57 trillion in NDFI loans, 5 quarters of FFIEC Call Report data.

Morgan Stanley projecting 8% default rate in direct lending. Investors demanding their money back. Which banks are most exposed? How thin are the reserves? The data is here - explore it yourself.

What you can do:

- Exposure levels and commitments broken by NDFI categories

- CET1 concentration and ACL reserve coverage across size segments

- Bank-level drill downs - click any bar to see the banks behind it

- Data explorer with filters across 55+ columns

- Methodology with MDRM codes. 7 levels of validation against FDIC and FRED

Full analysis decks inside the tool.

Plus - Dataset download. All 629 banks. All quarters. CSV.

tremor.tigzig.com ➔ US NDFI