US Consumer Lending Is Already at Crisis-Level Numbers - Without a Recession. NY Fed Q1 2026 Data.

Published: May 15, 2026

Latest NY Fed release for Q1 2026 came out two days back and shows a worsening trend.

Across every segment - auto, cards, mortgages, student loans - delinquencies are at or past 2007 pre-GFC levels. Auto has crossed the GFC peak itself. Cards are right there. Mortgage stock looks calm but the flow rate is cracking.

People are using HELOCs more, falling behind on them more. And home prices are down 9% from the 2022 peak...so the collateral itself is shrinking.

U-6 unemployment - the real labor measure including underemployed and marginally attached - back to pre-GFC 2007 levels. Home equity-rich share at the lowest since Q4-2021. Seriously underwater mortgages up in 45 states YoY.

This is what the data is saying. Nobody is calling it a crisis yet but the numbers are already there. As they were in the summer of 2007.

Deck below.

TREMOR Live Tool: tremor.tigzig.com ➔ US-Credit

Previous analysis: tigzig.com/analysis

US Consumer Lending - Crisis Without Recession

Browse the slides or download the PDF

Full Deck Content (Text Format)

Text below was extracted from the source deck. Chart visuals stay in the PDF and as slide images above the post.

US Lending Crisis - II

Amar Harolikar

Decision Sciences & Applied AISpecialist – Banking Analytics

14th May 2026

Tigzig.com

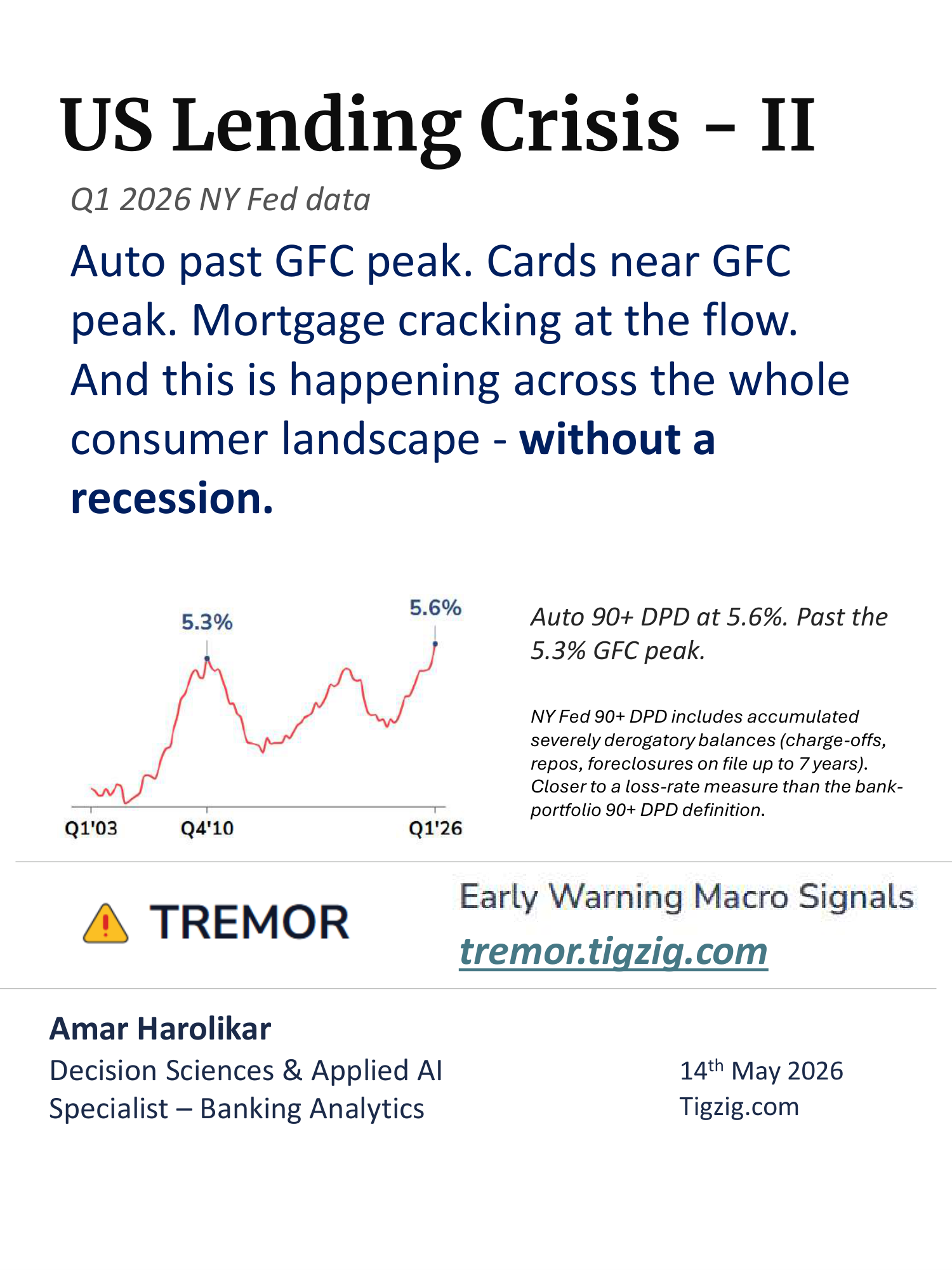

Q1 2026 NY Fed data

Auto past GFC peak. Cards near GFC peak. Mortgage cracking at the flow. And this is happening across the whole consumer landscape - without a recession.

Auto 90+ DPD at 5.6%. Past the 5.3% GFC peak.NY Fed 90+ DPD includes accumulated severely derogatory balances (charge-offs, repos, foreclosures on file up to 7 years). Closer to a loss-rate measure than the bank-portfolio 90+ DPD definition.

NY FED CONSUMER - ALL DEBT

Aggregate 90+ DPD at 3.4%. Already past the 3.1% pre-GFC Q3-2007 level. Steady climb over the last six quarters.

Source: NY Fed Consumer Credit Panel / Equifax via Tigzig Tremor platform

Note: NY Fed 90+ DPD is broader than the bank-portfolio definition - it includes accumulated severely derogatory balances (charge-offs, repos, foreclosures on file up to 7 years). Closer to a loss-rate measure.

NY FED CONSUMER - SEGMENT MIX

Stress is broad-based. Cards and auto are loudest. But mortgage at 1.1% is rising fast off a pandemic-distorted base - more on that ahead.

Source: NY Fed Consumer Credit Panel / Equifax via Tigzig Tremor platform

Note: NY Fed 90+ DPD is broader than the bank-portfolio definition - it includes accumulated severely derogatory balances (charge-offs, repos, foreclosures on file up to 7 years). Closer to a loss-rate measure.

NY FED CONSUMER - CREDIT CARDS

Cards at 13.1%, near 13.7% GFC peak. Different from 2008-09 - this time it has climbed without a recession.

Source: NY Fed Consumer Credit Panel / Equifax via Tigzig Tremor platform

Note: NY Fed 90+ DPD is broader than the bank-portfolio definition - it includes accumulated severely derogatory balances (charge-offs, repos, foreclosures on file up to 7 years). Closer to a loss-rate measure.

NY FED CONSUMER - AUTO LOANS

Auto at 5.6%. Past the 5.3% GFC peak. The first major consumer segment to break beyond GFC levels.

Source: NY Fed Consumer Credit Panel / Equifax via Tigzig Tremor platform

Note: NY Fed 90+ DPD is broader than the bank-portfolio definition - it includes accumulated severely derogatory balances (charge-offs, repos, foreclosures on file up to 7 years). Closer to a loss-rate measure.

NY FED CONSUMER - MORTGAGE (STOCK)

Mortgage 90+ DPD at 1.1%. Half the 2.2% pre-GFC level - on the surface, looks fine. But the pace of the rise is the story. Tripled from 0.37% in Q3-2022. Even adjusting for the CARES Act forbearance distorting that trough, the climb off pre-pandemic norms is real. 2006-07 also started calm. The flow rate next is what to watch..

Source: NY Fed Consumer Credit Panel / Equifax via Tigzig Tremor platform

NY FED CONSUMER - MORTGAGE (FLOW)

Straight-through flow rate - balance going Current to 90+ DPD in one quarter. Sudden distress, not normal early delinquency. At 0.26%, approaching the 0.35% pre-GFC level. Sharp climb in the last six months - the early-crack signal stock numbers miss.

Source: NY Fed Consumer Credit Panel / Equifax via Tigzig Tremor platform

NY FED CONSUMER - STUDENT LOANS

At 10.3%. The 2020-2023 trough was artificial - CARES Act paused federal student loan reporting. Now back on the pre-pandemic trajectory.

Source: NY Fed Consumer Credit Panel / Equifax via Tigzig Tremor platform

U-6 UNEMPLOYMENT

U-6 captures unemployed plus underemployed plus marginally attached. The real labor picture. At 8.2% - back to the pre-GFC 2007 starting level. Jobs side is already where it was before the last credit cycle broke.

Source: BLS via Tigzig Tremor platform

NY FED CONSUMER - HELOC

Tapping more, falling behind more.

Utilization at 42.6%, climbing every quarter since Q1-2023. HELOC at 7-8% is the cheapest credit left - with cards at 13% delinquency and 20%+ rates, the house is becoming the emergency fund.

Delinquency at 0.95% - 2.6x the Q2-2024 low. Still below the 1.2% pre-GFC level, but the trajectory is clear.

Source: NY Fed Consumer Credit Panel / Equifax via Tigzig Tremor platform

HE Revolving (HELOC) Utilization

HELOC Balances 90+ DPD (Stock)

HOME PRICES & EQUITY

Median price flat after the 2022 spike - down from $442.6K to $403.2K. Equity-rich share declining (46.2% to 43.3% YoY), seriously underwater up to 3.2% in 45 states. And the collateral itself is now weakening.

Source: FRED (Median Sales Price) via tremor.tigzig.com and ATTOM Q1-2026 Home Equity & Underwater Report

Equity-Rich Mortgages (% of mortgaged homes)

46.2%

Q1'25

44.6%

Q4'25

43.3%

Q1'26

Seriously Underwater (% of mortgaged homes)

2.8%

Q1'25

3.0%

Q4'25

3.2%

Q1'26

Median Sales Price of Houses Sold (USD)

WARNINGS

Jamie Dimon, CEO JPMorgan Chase

“I do believe that when we have a credit cycle, which will happen one day, losses on all leveraged lending in general will be higher than expected, relative to the environment. This is because credit standards have been modestly weakening pretty much across the board.”

Equifax Insights

“Credit risk dynamics are shifting as improvements in personal loans and private label delinquency are being countered by a rise in severe mortgage delinquency, alongside a worsening in subprime vintages for both Bankcard and unsecured personal loans through 2024.”

Auto is past GFC peak. Cards at GFC peak. Mortgage cracking at the flow. The setup is already worse than pre-GFC 2007.

And the worst impact of AI labor displacement, oil and inflation shocks, private credit stress and asset overvaluations is yet to play out.

Data & Tools

Primary Data Sources

NY Fed Consumer Credit Panel / Equifax

FDIC Statistics on Depository Institutions

NCUA Quarterly Aggregate FPR

FFIEC Call Reports (NDFI)

BLS - Bureau of Labor Statistics

TREMOR Platform - tremor.tigzig.com

4 modules. ~150 indicators. ~340 quarters of pooled history.

3-layer validation. 1,300+ automated cross-checks.

Time-series, cross-section, compare views.

Per-chart customization. PNG / TSV / CSV exports.