Dimon Was Right. More 'Cockroaches' Arrive. UK Lender MFS Collapses - $2.5B Exposure Across 12+ Global Banks and Credit Firms.

Published: May 18, 2026

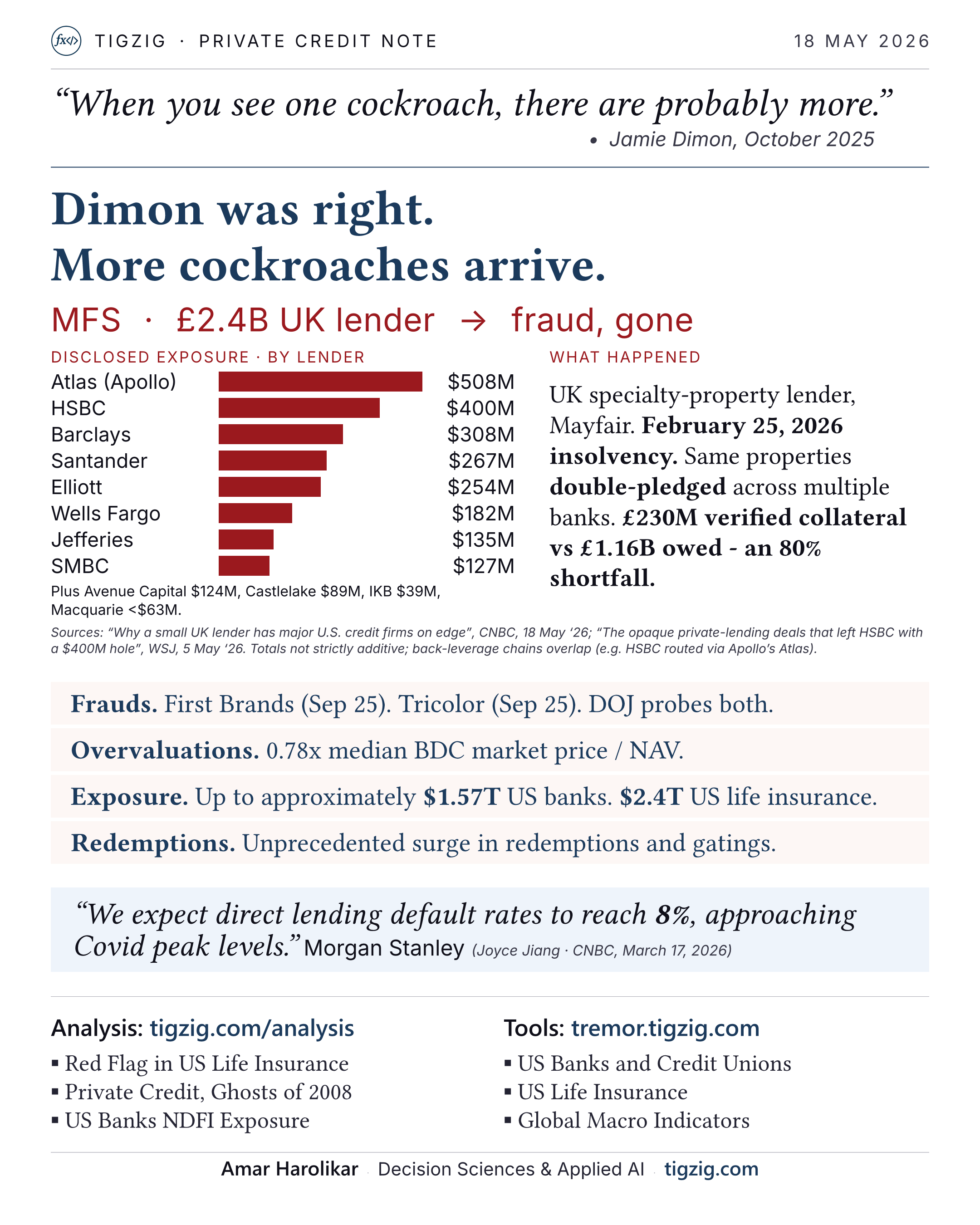

UK lender MFS collapsed in February. Over $2.5B of exposure spread across 12+ global banks and credit firms - Barclays $308M, HSBC $400M, Atlas/Apollo $508M, Santander $267M, Elliott $254M, Wells Fargo $182M. Plus Jefferies, Avenue Capital, SMBC, Castlelake, Macquarie, IKB.

£2.4B loan book. Allegations of fraud and double-pledging. £230M of verified collateral against £1.16B owed - an 80% shortfall.

And the structure makes it worse. HSBC's exposure ran through Apollo's Atlas, which lent to Zircon Bridging, which funded MFS loans. Banks lending to private credit firms lending to specialty lenders. Nobody really knew the full chain.

Morgan Stanley (Mar'26) expects direct lending default rates to hit 8%, approaching Covid peak levels.

Analysis: tigzig.com/analysis

Tools: tremor.tigzig.com · tigzig.com

Full Deck Content (Text Format)

Text below was extracted from the source one-pager (HTML/typst). The image above is the visual.

TIGZIG · Private Credit Note · 18 May 2026

"When you see one cockroach, there are probably more." — Jamie Dimon, October 2025

MFS · £2.4B UK lender → fraud, gone

What happened. UK specialty-property lender, Mayfair. February 25, 2026 insolvency. Same properties double-pledged across multiple banks. £230M verified collateral vs £1.16B owed — an 80% shortfall.

Disclosed exposure by lender

| Lender | Exposure |

|---|---|

| Atlas (Apollo) | $508M |

| HSBC | $400M |

| Barclays | $308M |

| Santander | $267M |

| Elliott | $254M |

| Wells Fargo | $182M |

| Jefferies | $135M |

| SMBC | $127M |

Plus Avenue Capital $124M, Castlelake $89M, IKB $39M, Macquarie <$63M.

Sources: "Why a small UK lender has major U.S. credit firms on edge", CNBC, 18 May 2026; "The opaque private-lending deals that left HSBC with a $400M hole", WSJ, 5 May 2026. Totals not strictly additive; back-leverage chains overlap (e.g. HSBC routed via Apollo's Atlas).

The pattern, stacked

- Frauds. First Brands (Sep 25). Tricolor (Sep 25). DOJ probes both.

- Overvaluations. 0.78x median BDC market price / NAV.

- Exposure. Up to approximately $1.57T US banks. $2.4T US life insurance.

- Redemptions. Unprecedented surge in redemptions and gatings.

Default outlook

"We expect direct lending default rates to reach 8%, approaching Covid peak levels." — Morgan Stanley (Joyce Jiang · CNBC, March 17, 2026)

Further reading

Analysis: tigzig.com/analysis

- Red Flag in US Life Insurance

- Private Credit, Ghosts of 2008

- US Banks NDFI Exposure

Tools: tremor.tigzig.com

- US Banks and Credit Unions

- US Life Insurance

- Global Macro Indicators

Amar Harolikar · Decision Sciences & Applied AI · tigzig.com