Bank Loss Rates Look Calm. The Stuff Underneath - Consumer, Private Credit, Non-Banks - Says Otherwise.

Published: June 4, 2026

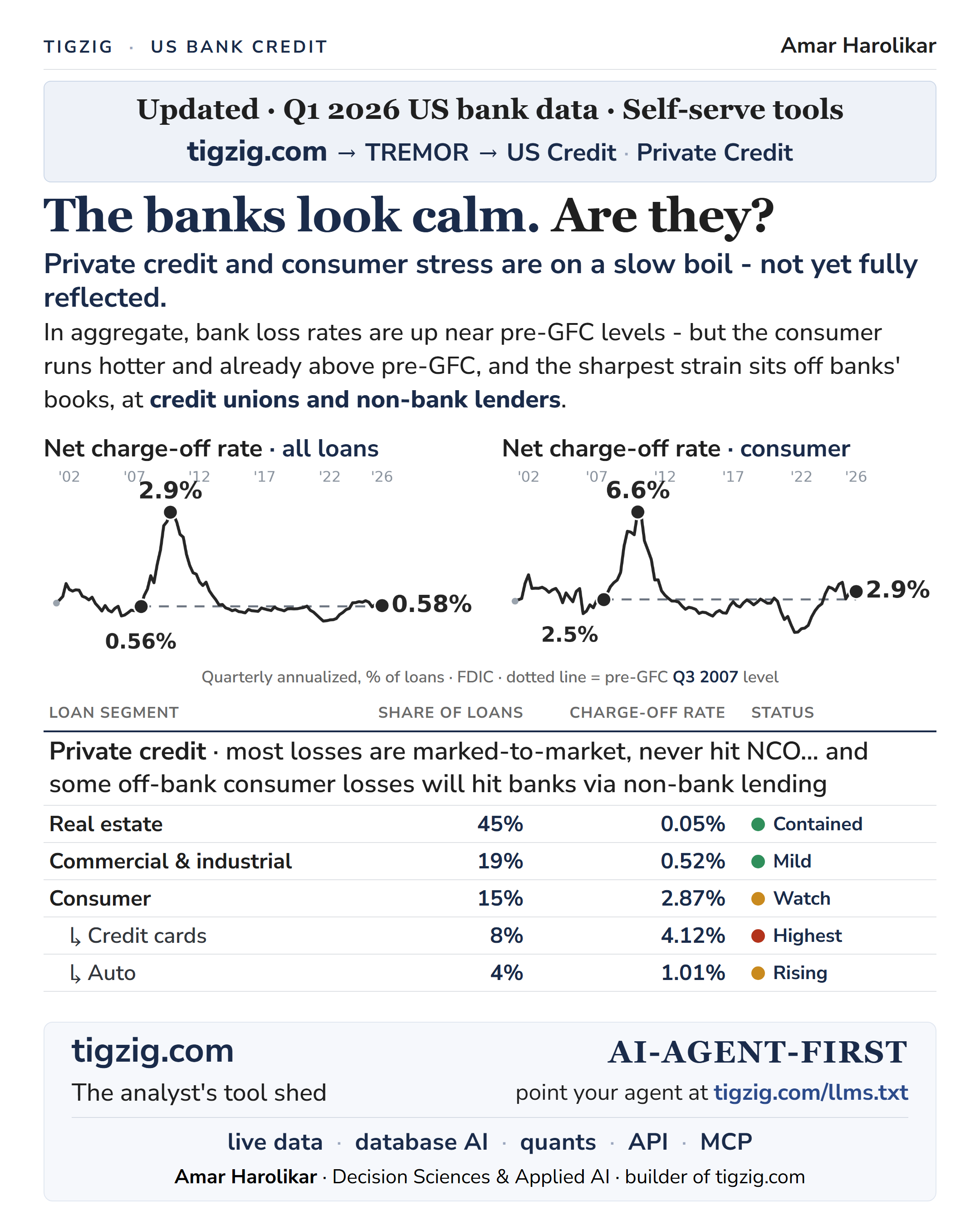

The loss rates at banks look calm. But there's a storm brewing underneath - from the consumer, private credit and non-bank lending.

US bank net charge-offs at 0.58% in Q1 2026... right at pre-GFC, miles under the GFC peak. Pull the consumer book out and it's already running hotter than pre-GFC - 2.9% vs 2.5% in 2007. Cards the highest. Auto rising.

And the sharpest stress sits off the bank books. Most private credit losses are marked-to-market... they hit P&L direct, never show as a charge-off.

From my earlier analysis - credit unions and non-bank lenders carry the weakest consumer paper... which loops back to banks via their non-bank and private credit lines.

The bigger worry - the macro is weak. Unemployment, savings rate, producer inflation, oil and gas all the wrong way. Consumers stretched thin.

The bank NCO looks calm. The stuff it can't show says otherwise.

-----

Analysis supported by TREMOR, my own self-serve analytics tool.

Tool + earlier deep dives: tigzig.com → TREMOR