ECB Stress-Tested Private Credit. Pensions Worst at 6% of Assets. Almost All the Damage Is the Wider Market Crash It Sets Off.

Published: June 2, 2026

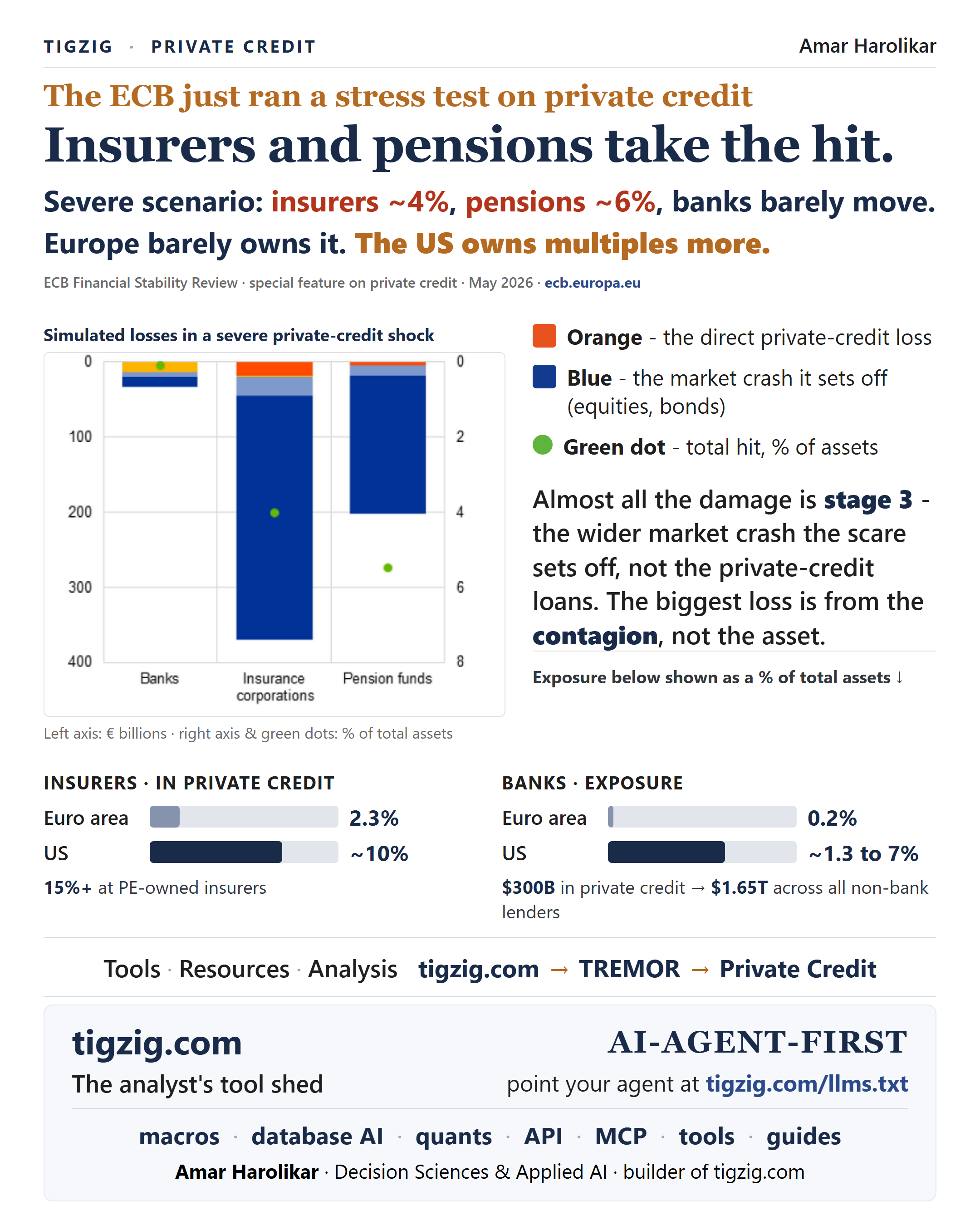

The ECB just stress-tested private credit. Insurers and pensions take the hit... pensions worst, around 6% of assets in the severe scenario. And that's for the Euro area which has a tiny share... US has multiple times the exposure.

They walked it through three stages.

Stage 1 - direct private credit losses.

Stage 2 - the same shock spreading to leveraged loans and high-yield bonds.

Stage 3 - a tail-risk assumption... equities crash 30%, high-yield bonds reprice 25%, money runs out of private credit funds.

Almost all the damage is stage 3... the wider market crash the scare sets off, not the private credit loans themselves.

Contagion is bigger than the asset... we have seen in earlier crises.

As for tail risk... GFC 2008 was supposed to be tail risk by most... till Lehman happened.

And this time around, given the simultaneous multiple pressures across global economies, from experience with both the dot-com crash and the GFC... I would not treat this as just tail risk.

Read analysis here: tigzig.com/analysis

Track Private Credit stress here:

tigzig.com → TREMOR → PRIVATE CREDIT

ECB Report: "Stress in global private credit markets and its implications for euro area financial stability"

Link: ecb.europa.eu

Part of ECB Financial Stability Review, May 2026.