NIFTY50 - 30 Day Forward Return Analysis Feb 2008 to 2026 - Claude in Excel with Python, Lambdas and Advanced Formulas

Published: February 11, 2026

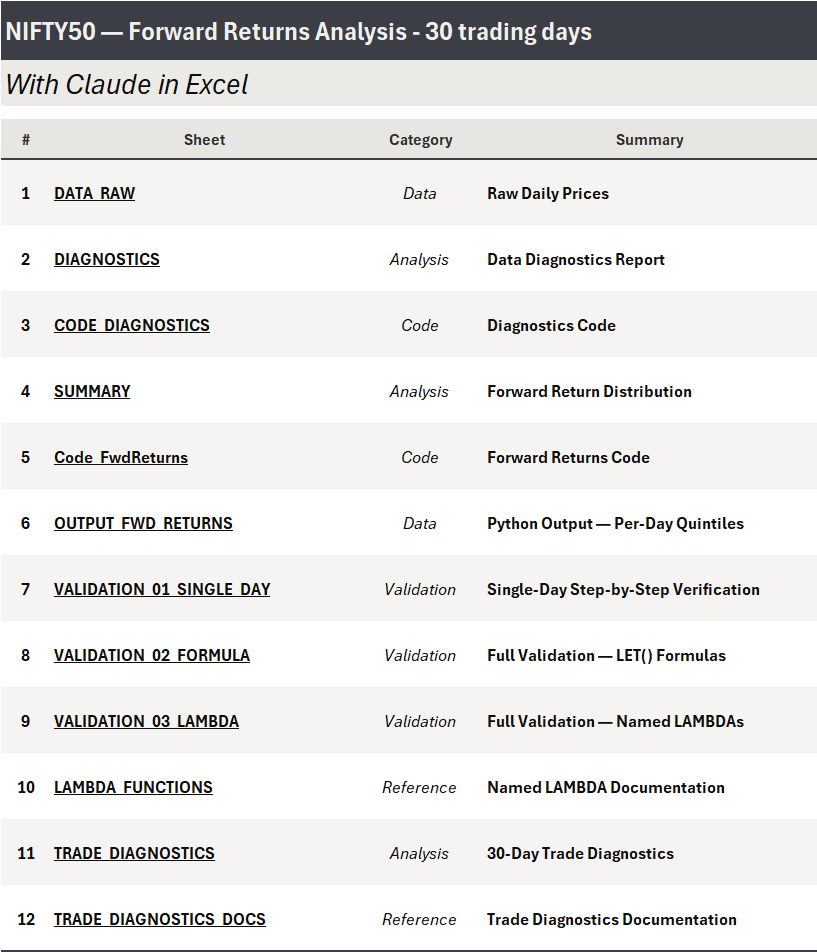

File shared + Power User Guide for Claude in Excel.

Analysis

For each Nifty50 trading day, compute 30 forward returns (Day 0 to Day 1, Day 0 to Day 2... Day 0 to Day 30). From those 30 returns - quintile cuts (P20, P40, P50, P60, P80) plus positive/negative day counts. And confidence intervals assuming normality for the time being. Then 30-day rolling diagnostics - max consecutive positive/negative streaks, max drawdown and runup %, days to max drawdown/runup, recovery days long and short.

How Claude handled it

Quintile calculation in Python first, then validate with manual formula for a single day, then validate with LET + SEQUENCE, then setup a named LAMBDA function for reuse. Trade diagnostics using MAP, REDUCE and SCAN with LAMBDA - these walk through 30-day forward windows item by item. Had it setup documentation sheets ...plus a hyperlinked index sheet at start.

Whole thing took just ~2.5 hours over two sessions. About an hour brainstorming and discussion, rest in processing, redoing, formatting. All done per instructions, but you need to be very clear ....and very granular sometimes in what you want it to do.

Still WIP

3 validations done for quintile cuts. Diagnostics need summarizing with distributions and confidence intervals, then full validation via Python recreation. After that - Gold, Oil & S&P 500 .. then add technicals ...then a regression...mostly quantile ...but yet to think through.

For traders

These are closing rates. Good for quick diagnostics only. Intraday prices needed for practical work. And for actual setups and backtesting, Claude Code / Scripts / Notebooks might be more efficient.

Be aware:

- Heavy excel work is also token heavy

- Python code is reconstructed code, not the code snippets it actually ran.

Resources

- Workbook: NIFTY50 Forward Return Analysis

- Power user guide - Claude in Excel: Power User Guide to Claude in Excel & PowerPoint - 26 Working Tips

- Get aligned price data: Portfolio Analysis Suite