Are We Headed for Stagflation-Lite

Published: March 28, 2026

Stagflation-Lite - that's where several macro signals are pointing right now. The Fed is trapped. Can't cut - inflation risk too high. Can't hike - jobs too weak. Oil shock is not going to wear off soon. That's the bind.

Bond markets pricing in high inflation. US 10Y yield at 4.4%. Germany Bund moving the same way. PPI at 3.4% with the oil shock not yet in the data. GDP revised to 0.7%. Consumer sentiment 7th lowest in 40 years. Moody's recession odds at 48.6%.

I track this through TREMOR - macro early warning dashboard at tremor.tigzig.com. Built by analyst...for analysts...free...no login. Full analysis in the slides.

Negative shocks continue, things stay difficult. A series of positive shocks and it can all change on a dime. Seen it happen both ways.

My forecast...is always 100% correct - it can go up, it can go down, or it can go sideways. Have a setup ready for each...once a trader, always a trader...

Are We Headed for Stagflation-Lite

Browse the slides or download the PDF

Full Deck Content (Text Format)

Text below was extracted from the source deck. Chart visuals stay in the PDF and as slide images above the post.

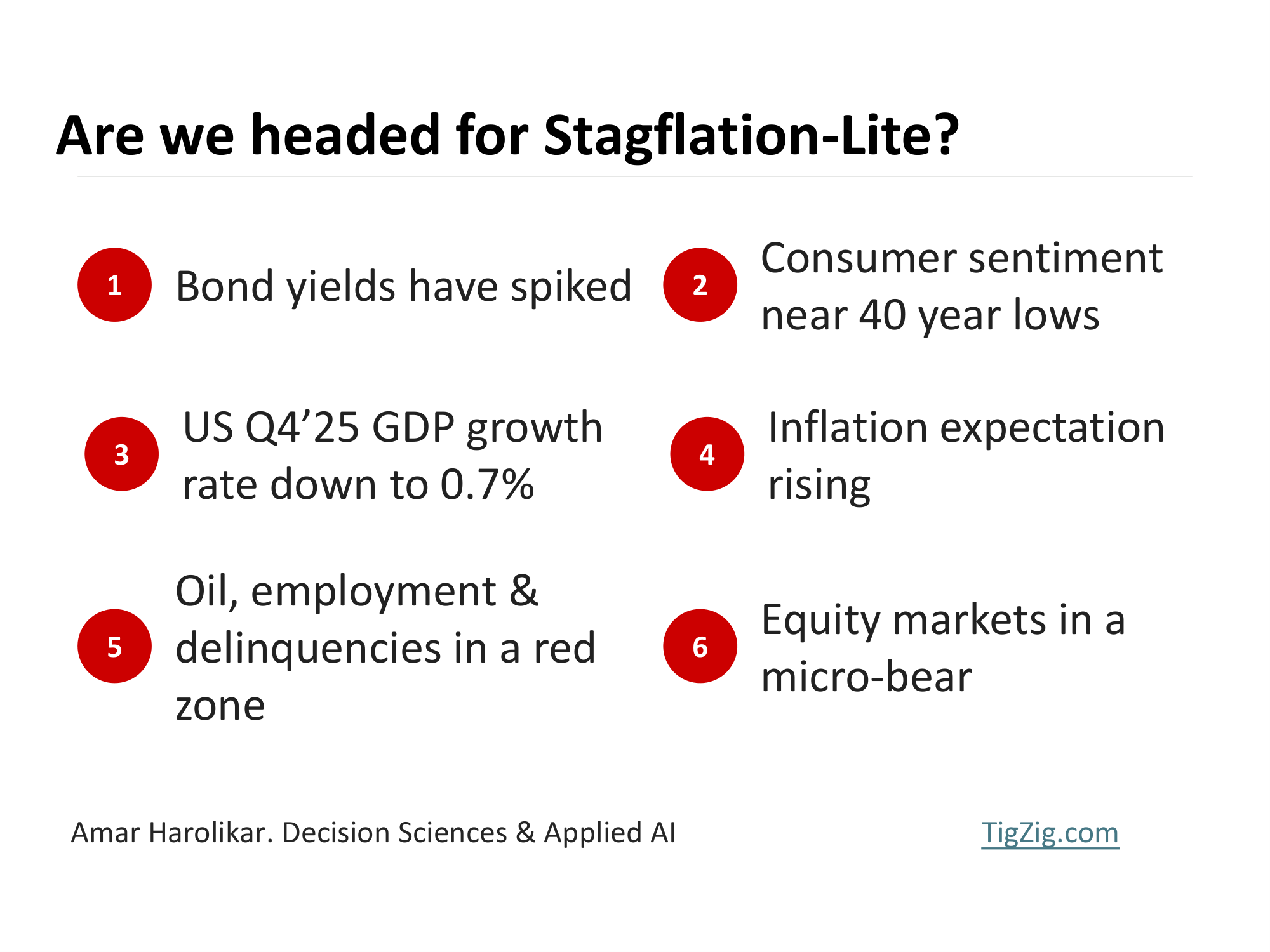

Are we headed for Stagflation-Lite?

1

Bond yields have spiked

2

Consumer sentiment near 40 year lows

3

US Q4’25 GDP growth rate down to 0.7%

4

Inflation expectation rising

5

Oil, employment & delinquencies in a red zone

6

Equity markets in a micro-bear

TREMOR –monitor early warning signals

Built by analyst – for analysts

Cockpit view of key macros + News

Live at: tremor.tigzig.com

Here’s what the TREMOR charts are telling us

Bond markets pricing in high inflation expectation

US Past 20 Years

Past 6 Months

US Treasuries 10Y Yield

Germany 10Y Bund Yield

Institutional and bond desk expecting higher inflation. Which make the current yields unattractive, causing sell-off and pushing yields higher. Becomes self fulfilling – the expectation itself create outcome in bond markets increasing risk to real economy CNBC – Rising European Yields, Bloomberg Podcast

US Feb’26 PPI annual inflation at 3.4%, higher than expected

US Past 20 Years

The producer price index is a measure of pipeline costs that producers receive for their products and an early indicator of consumer inflation. The annual inflation rate was at 3.4%, highest in past year. And the oil shock is yet to be baked in

Consumer sentiments running abysmally low

Michigan Consumer Sentiment results released March 27 came in at 53.3 amongst the lowest reading (7th lowest) in past 40 years

US GDP growth rate revised to 0.7%

The first revision of GDP on13th March 2026 was a 50% lower than the previous 1.4% and below Dow Jones consensus forecast of 1.5% CNBC (Seasonally & inflation adjusted Annualized QoQ growth rate)

Oil, unemployment and delinquencies in red zone

Brent continues to be above $100 and even when the Iran war ends and prices fall, the transmission won’t be instant. Some capacities may get online in months, others might take years. All while pressures continue on employment side and rising delinquencies.

Economists raising odds of a recession

Moody’s Analytics’ model has raised its recession outlook for the next 12 months to 48.6%. Goldman Sachs boosted its estimate to 30%. Wilmington Trust has the odds at 45%, while EY Parthenon has it at 40%, with the caveat that “those odds could rapidly rise in the event of a more prolonged or severe Middle East conflict.”

In normal times, the risk for a recession in any given 12-month span is around 20%. So while the current predictions are hardly certainties, they signify elevated risk.

“I’m concerned recession risks are uncomfortably high and on the rise,” said Mark Zandi, chief economist at Moody’s Analytics. “Recession is a real threat here.”

Recession odds climb on Wall Street as economy shows cracks beneath the surface CNBC, March 25, 2026

Equity markets entering micro-bear territory

Key equities dropped ~10% the past month from their recent highs

Are we heading for a stagflation like scenario?

Stagflation = High Inflation + Stagnant Growth

Expectation of higher inflation

Expectation of lower growth

Continuing negative shocks

=

Higher probability of stagflation like scenario

or 'Stagflation-Lite'

Previous Analysis

Are we staring into face of a full bear market?US Banks & Non-Bank Lending - How Deep is the Exposure? Is there a Systemic Risk?Structural Weakness IntensifyingPrivate Credit - The $2.7 Trillion Shadow Lending Market Is Showing Cracks