Structural Weakness Intensifying

Published: March 20, 2026

3 major data points in 3 days. All pointing the same direction. US macro signals flashing red - and the ripple effects are global.

US Feb payrolls: minus 92K. Against expectations of 59K rise. 5th time in 9 months the economy lost jobs.

PPI Core: 3.87%. Producers paying more - and the March oil shock hasn't even hit the data yet.

Fed: Held at 3.5-3.75%. Can't cut because inflation. Can't hike because employment.

Brent crude nearly doubled in 3 months. Delinquencies past COVID highs. Retail sales declining. Yield curve flattening with both ends rising.

I track key macro signals daily on Tremor (tremor.tigzig.com).

Right now many are flashing stress simultaneously.

Structural Weakness Intensifying - March 2026

Browse the slides or download the PDF

Full Deck Content (Text Format)

Text below was extracted from the source deck. Chart visuals stay in the PDF and as slide images above the post.

You don’t know who’s been swimming naked until the tide goes out. - Buffet

Ghosts of 2008

Is Private Credit going to be the straw that broke the Camel’s back

What is Private Credit & Direct Lending

2025E Private Lending ~2.7T & direct lending ~1.4T

Direct Lending > 50% of all private credit

Evolution of Direct Lending - Morgan Stanley – 2026Private credit investments: 'Some caution is reasonable,' advisor says

Private credit is lending outside the traditional banking system - private lenders originate loans directly with borrowers

Post-2008, banks retreated from lending to smaller firms. Direct lending filled that gap for middle market companies

Banks are still exposed - they fund private lenders (BDCs)

Retail/HNW investors exposed via BDCs, new private credit ETFs & Pension fund investments

“A significant private credit shakeout on par with Covid losses is coming” – Morgan Stanley

Private credit shakeout matching Covid losses coming, Morgan Stanley saysEvolution of Direct Lending - Morgan Stanley - 2026

“In our view, AI disruption will be a meaningful catalyst to drive defaults higher in direct lending… Overall, we expect the direct lending default rates to reach 8%, approaching Covid peak levels”

- strategist Morgan Stanley Joyce Jiang (as reported by CNBC)

Premise: New technology & AI ➜ erode demand for software services ➜ hurt lenders

Morgan Stanley estimates that ~26% of direct lender portfolios (BDCs) and ~19% of private credit CLOs are exposed to software - a sector highly vulnerable to AI disruption

Investors in private credit demanding their money back

Blackstone's flagship private credit fund posts first monthly loss in over three years | ReutersWhy Wall Street is calling out ‘echoes’ of the 2008 financial crisis | CNN BusinessAfter pouring billions into private credit, many investors want out

Blackstone, the private equity giant: $3.8 billion in redemption requests. At least 25 senior leaders from across the firm pitched in some $150 million from their own wallets .

BCRED, Blackstones flagship private credit fund posted its first monthly loss of 0.4% in more than three years in February, it’s first since September 2022 ,when it posted a loss of 1.3%.

Blue Owl - hit with withdrawal requests. Halts redemptions and liquidates assets to repay.

“When you see one cockroach, there are probably more… Everyone should be forewarned on this” Jamie Dimon

Why Jamie Dimon is warning of ‘cockroaches’ in the US economy | CNN Business

Beyond software, the other stress point is subprime auto lending. In 2008 it was toxic mortgages - today the red flag is car loans Tricolor Holdings (subprime auto lender) went bust Sep 2025. Even JPMorgan took a $170M hit from this single bankruptcy First Brands (auto-parts) filed Chapter 11 with ~$2.3B in hidden loans. DOJ opened a criminal probe - echoes of Lehman

Dimon’s point: these may be isolated, but in a downturn more will surface - “when you see one cockroach, there are probably more”

Are Car Loans the next ‘toxic mortgages’

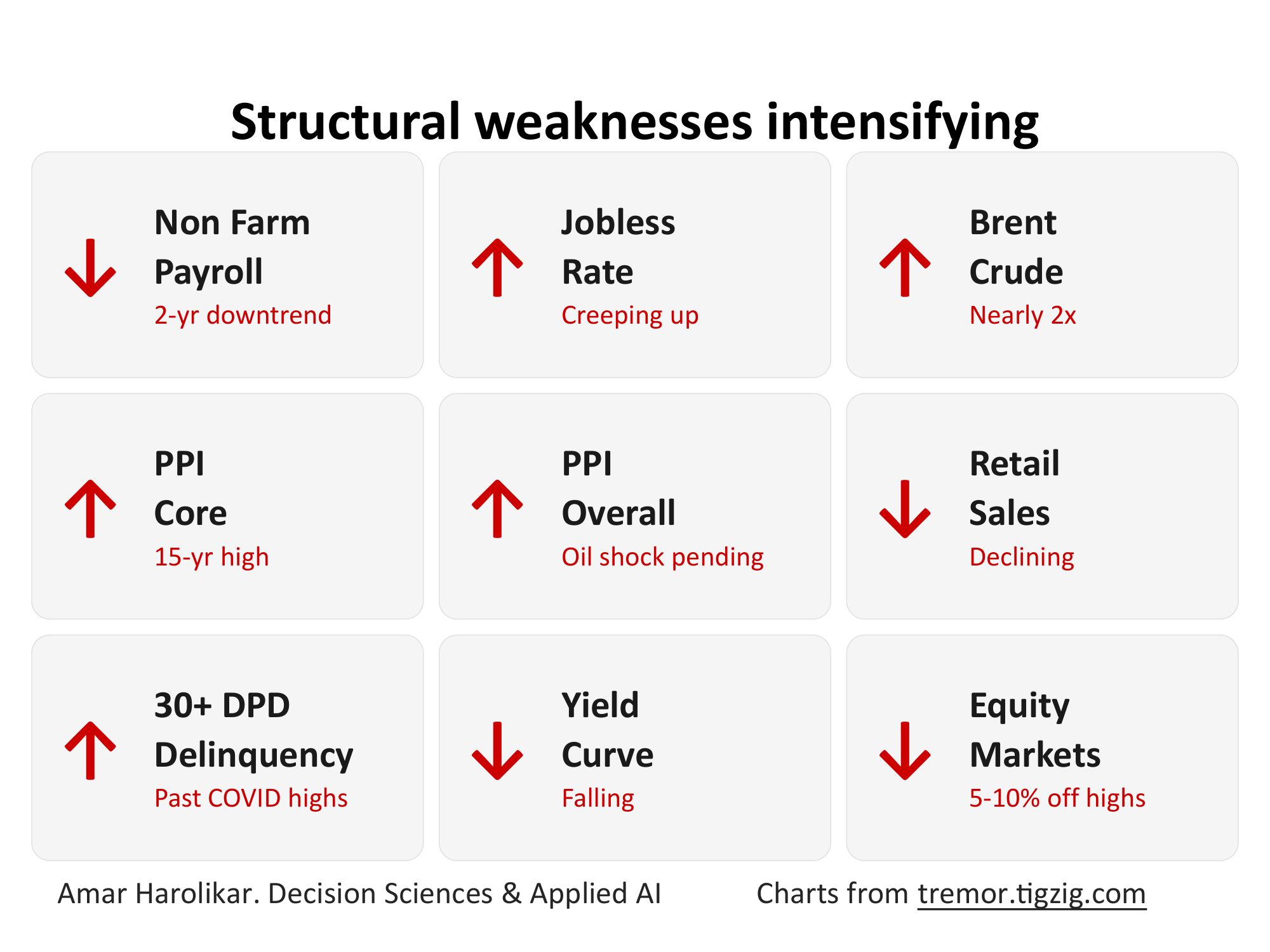

Structural weaknesses intensifying

↓

Non Farm Payroll

2-yr downtrend

↑

Jobless Rate

Creeping up

↑

Brent Crude

Nearly 2x

↑

PPI Core

15-yr high

↑

PPI Overall

Oil shock pending

↓

Retail Sales

Declining

↑

30+ DPD Delinquency

Past COVID highs

↓

Yield Curve

Falling

↓

Equity Markets

5-10% off highs

Unemployment creeping up steadily the past 2 years

Past 20 Years

Brent moving towards 2008 territory

Nearly doubled in past 3 months – supply shock as strait of Hormuz remains closed

Past 25 Years

US 30+ DPD has already crossed the COVID highs

Past 20 Years

Markets are already pricing in the weakness

S&P 500 is down ~5% from its Jan 2026 high

Nifty 50 is down ~10% from its Jan 2026 high

DAX is down ~8% from its Jan 2026 high

No predictions.

Just data. Tracked daily

10 Signals – all pointing in same direction