BIS, the Central Bank of Central Banks, Just Red-Flagged the AI Boom. Railway Mania, Roaring 20s, Dotcom - Same Chart.

Published: June 30, 2026

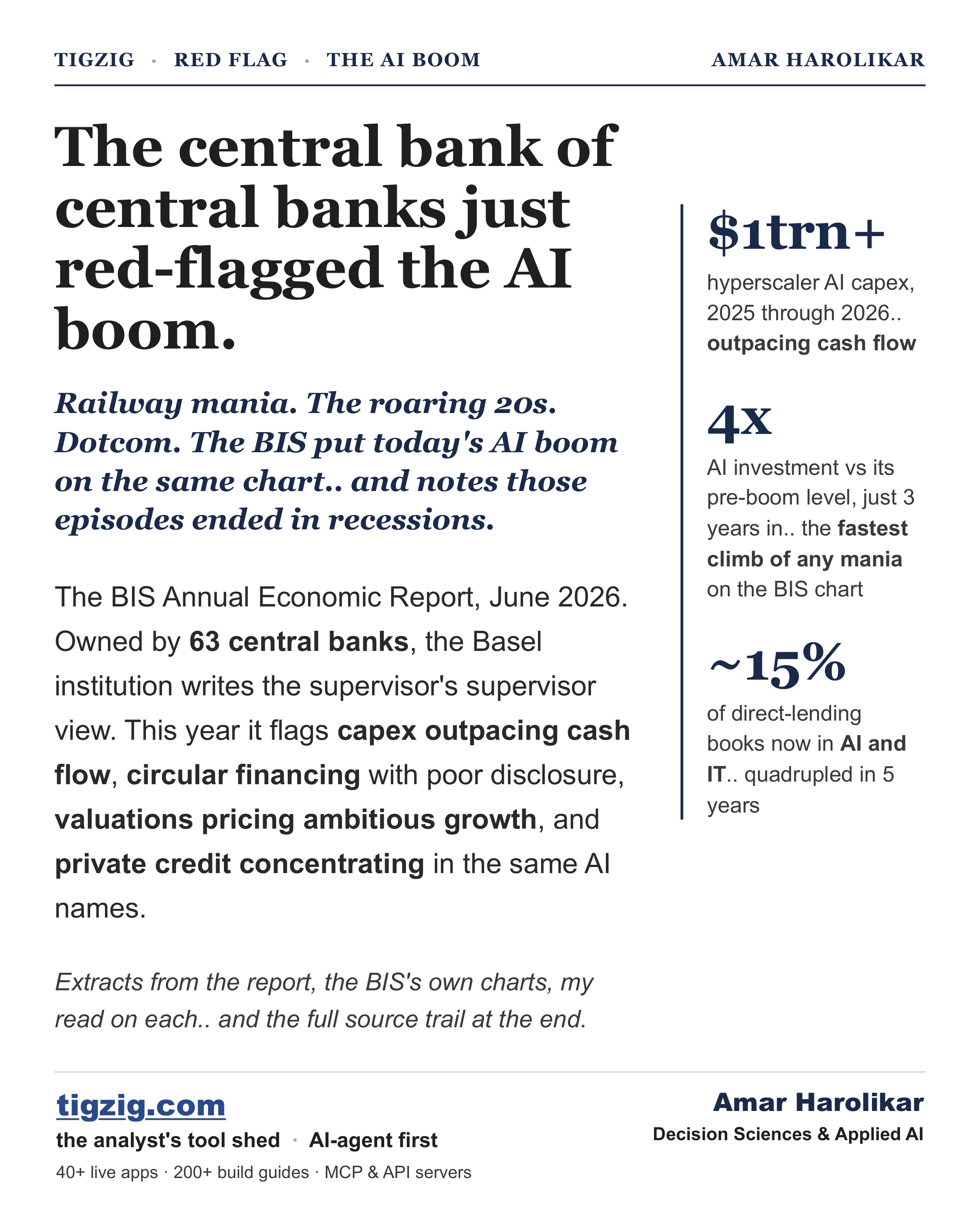

BIS, the central bank of central banks, just red-flagged the AI boom. I have been calling the 'Irrational Exuberance' since March when markets were making new highs. And the regulators have been calling it too, each in their own careful language.

Bank for International Settlements (BIS), owned by 63 central banks, has put it on the record in its Annual Economic Report. And the wordings are a shout rather than a whisper.

It charts today's AI boom next to railway mania, the roaring 20s and dotcom. Its words: those episodes attracted "capital in excess of what commercial returns could ultimately justify".. and ended in economy-wide recessions.

Also in the report:

- $1trn+ hyperscaler AI capex, outpacing free cash flow, part funded by debt

- Circular financing, risks of "the same asset being pledged multiple times"

- Valuations pricing growth above what these firms have ever delivered

- The bust is modeled in print.. sector surplus goes negative in the BIS adverse scenario

- Direct lenders quadrupled AI/IT lending to ~15% of books

Charles Mackay wrote the book on market madness 185 years ago, titled very appropriately: 'Extraordinary Popular Delusions and the Madness of Crowds'

"We find that whole communities suddenly fix their minds upon one object, and go mad in its pursuit; that millions of people become simultaneously impressed with one delusion... Sober nations have all at once become desperate gamblers, and risked almost their existence upon the turn of a piece of paper."

Source & my earlier analysis

- BIS Annual Economic Report, June 2026 - https://lnkd.in/dRAfec4z

- Irrational Exuberance, S&P at 7,400 (17 May) - tigzig.com/post/sp500-irrational-exuberance-7400-may2026

- Early warning: another full bear (14 Mar) - tigzig.com/post/tremor-macro-signals-march-2026

- Is Private Credit Turning Into a Lemon? - tigzig.com/post/private-credit-market-for-lemons-may2026

If you only read 8 pages of the 133

Pages 19 to 26. "AI progress and investment boom under pressure" plus "Financial vulnerabilities as amplifiers". Graphs 10 to 14 have the whole story.. the mania chart, the circular financing, the private credit concentration. Box C has the demand bottleneck model: every displaced worker is also a lost consumer.

A credit investor's read on the same report

For a credit investor's read on the same report: Ashwinder Singh Bakhshi, 22 years in fixed income markets, Former MD, Barings.. he picked up the same BIS sentence.. "same asset being pledged multiple times".. and takes it where a lender would: the collateral behind your loan may already sit behind someone else's, and you find out whose it really is in default, not before. He calls it phantom collateral.

BIS Report Hints at the Existence of Phantom Collateral - Ashwinder Singh Bakhshi

Same discipline applied to Korea

His Korea piece applies the same discipline to a whole market. KOSPI doubled in six months while the foreign institutions who know it best sold W148 trillion into the rally, retail absorbed it on record margin debt.. and the biggest forced sellers now sit above the market, not below it. "A distribution with excellent PR," as he puts it.

Margin Called: The W148 Trillion Exit Behind Korea's 100% Rally - Ashwinder Singh Bakhshi

Full Deck Content (Text Format)

The 10-slide deck as accessible text - indexable by search engines and AI agents.

Slide 1 - Cover

Red Flag - The AI Boom. The central bank of central banks just red-flagged the AI boom. Railway mania. The roaring 20s. Dotcom. The BIS put today's AI boom on the same chart and notes those episodes ended in recessions.

- $1trn+ hyperscaler AI capex, 2025 through 2026, outpacing cash flow.

- 4x AI investment vs its pre-boom level, just 3 years in - the fastest climb of any mania on the BIS chart.

- ~15% of direct-lending books now in AI and IT, quadrupled in 5 years.

The BIS Annual Economic Report, June 2026. Owned by 63 central banks, the Basel institution writes the supervisor's supervisor view. This year it flags capex outpacing cash flow, circular financing with poor disclosure, valuations pricing ambitious growth, and private credit concentrating in the same AI names.

Slide 2 - The story in one page

Six red flags, spread quietly across eight pages of a 133-page flagship report.

- The parallel: AI boom charted next to canal mania, railway mania, roaring 20s, dotcom - all ended in recessions.

- The money: $1trn+ hyperscaler capex outpacing earnings and free cash flow; firms now issuing debt to fund it.

- The circular web: Circular financing, poorly disclosed deals, and risks of the same asset pledged multiple times.

- Valuations: Stocks pricing growth above what these firms have ever delivered; risk premia compressed to complacency levels.

- Private credit: Direct lenders quadrupled AI/IT lending to ~15% of books; multiple funds stacked on the same software borrowers.

- Labour: Firms signalling automation and labour substitution on earnings calls; AI-exposed sectors already hiring less.

Source: BIS Annual Economic Report, June 2026, Chapter I, pages 19 to 26.

Slide 3 - Railway mania, the 20s, dotcom.. and now AI

The BIS drew the chart itself. The black line is the AI boom - the steepest climb of the five.

"..a genuine technological breakthrough that attracted capital in excess of what commercial returns could ultimately justify. These episodes ended with an eventual reversal in investment, inducing economy-wide recessions."

"The scale and pace of the current AI investment boom.. bear resemblance to these precedents."

My read: the placement is the statement. A central bank institution does not put your boom on a chart with four historical manias by accident.. and the AI line is outpacing all four.

Source: BIS Graph 11, page 23.

Slide 4 - The trillion is outrunning the cash

Capex past free cash flow, funded with debt.. and the BIS models the whole sector going underwater.

- $1trn+ five largest hyperscalers, AI capex 2025 through 2026.

- $3-4trn the 2030 projection the BIS cites, from Nvidia's CEO.

- Negative where sector net economic surplus lands in the BIS adverse scenario.

"..capex plans are running past earnings and the free cash flow of these firms, leading some to issue debt to raise additional financing."

"Disappointment in returns could trigger a sudden pullback in financing and turn the capex boom into a protracted investment bust, with potential knock-on effects on financial conditions."

My read: the BIS built a formal model of the AI capex race.. and the sector's surplus goes negative in the adverse case. A stress test of the boom itself, in the flagship report.

Source: BIS pages 22 to 23 and Graph 11.

Slide 5 - The circular web nobody can see into

Chip makers fund AI labs. AI labs buy chips. The revenue is the investors' own money coming back.

"The terms of such deals are typically poorly disclosed, with risks of the same asset being pledged multiple times."

"..a complex web of private arrangements that accounts for a sizeable share of sector-wide financing and forward revenue."

My read: "same asset pledged multiple times" is 2008 language. In 2008 it appeared in the post-mortems. This time it is in print before the event.

Source: BIS Graph 13, page 25.

Slide 6 - Valuations pricing the impossible

Implied growth above anything these firms have ever delivered.. held by households at record exposure.

"Implied growth rates often exceed even the elevated growth that some of the technology firms have delivered in their relatively short lifetimes."

Risk premia point to "growing investor complacency and reduced compensation for risk-bearing." US stocks are ~64% of the MSCI Global index.. "A major equity market correction could have larger macroeconomic consequences today than in the past."

My read: the same setup I documented in my Irrational Exuberance brief in May.. CAPE at 39.6, the second highest in 145 years. The BIS now makes the macro case for why that matters.

Source: BIS Graph 12, page 24.

Slide 7 - Private credit is stacked on the same bet

The opaque lenders quadrupled their AI exposure.. and the BIS says the stress has already started.

- Direct lending funds have quadrupled lending to AI and IT in five years, to ~15% of portfolios.

- Larger loans, similar terms, "raising questions about lending standards and risk pricing."

- Stress is visible now: retail-facing funds forced to liquidate assets under redemptions.

- Contagion path: banks' "growing and opaque exposure" to the funds.. and "the real economy implications could be substantial."

My read: the Bank of England already asked whether private credit is a "market for lemons".. record 6.0% defaults, a KKR fund rescue, a DOJ valuations probe, all covered in my dispatches. The BIS just wired that market to the AI boom.

Source: BIS Graph 14, page 26.

Slide 8 - Every displaced worker is a lost consumer

The quiet chapter: firms are telling investors they will automate.. and the BIS models where that leads.

Unlike past technologies, AI "competes directly with human cognitive abilities, possibly narrowing the scope for workers to move up the value chain."

The BIS "demand bottleneck" scenario: "Since every displaced worker is also a lost consumer, the spending that rewards innovation eventually shrinks".. growth ends up below trend, from automation itself.

My read: productivity gains of 20 to 50% at task level are real.. I build with these tools daily. The question the BIS puts on the table: who buys the output when the workers who consumed it are gone?

Source: BIS Graph 10, page 22 and Box C.

Slide 9 - The regulators have stopped whispering. They are now shouting.

- Bank of England: a possible "market for lemons."

- ECB: US private credit as a spillover risk.

- IMF, FSB, OCC, the Fed.. each flagged a piece of it this year.

Each of those was a whisper between the lines. A flagship annual report that charts the AI boom next to railway mania, models the capex bust, and names the circular financing.. that is the shout.

I have been documenting this same pattern since March.. exuberance, credit, opacity. The supervisors' supervisor just put it on the record.

Slide 10 - Method & Sources

BIS Annual Economic Report, June 2026. Released 28 June 2026. 133 pages. This deck draws on Chapter I - "AI progress and investment boom under pressure" and "Financial vulnerabilities as amplifiers", pages 19 to 26, Graphs 10 to 14 and Box C. All charts on these pages are reproduced from the report.

My earlier calls:

- Early warning: another full bear? (14 March 2026) - the first call, published while markets were making new highs. CAPE at 40-year highs, gold vertical, crude towards 2008 levels, US delinquencies past COVID highs. Tremor macro early-warning signals.

- S&P 7,400. Irrational Exuberance (17 May 2026) - CAPE 39.6, second highest in 145 years. The last two times this setup held, the index halved. The valuation brief this BIS chapter now echoes.

- Is Private Credit Turning Into a Lemon? (May 2026) - Bank of England's "market for lemons" warning, the record 6.0% default rate, the FS KKR rescue, the DOJ valuations probe. Fourth dispatch in my private credit series.

Published for informational and educational purposes only. Reflects the author's analysis of publicly available data. Views in the BIS Annual Economic Report are those of the BIS; this is commentary on that report, with extracts reproduced with attribution. Nothing here is investment advice. Verify all data independently.