Euro-Area NPLs Look Calm. Split by Bank Size, the Small-Bank Corporate Book Is at 5.16% and Climbing.

Published: June 19, 2026

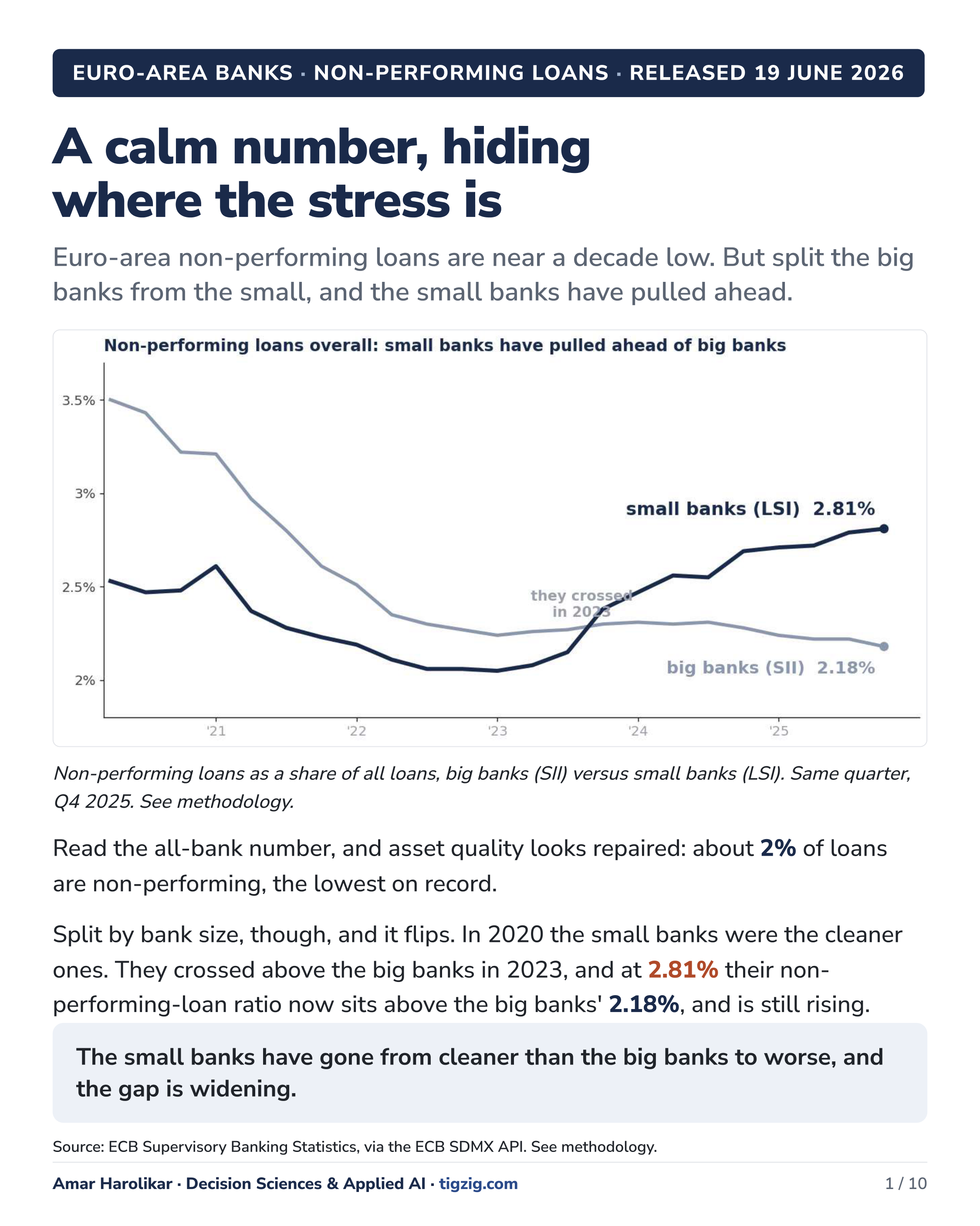

Euro-area non-performing loans are near a decade low. The headline looks peaceful. Split the banks by size, though, and the calm cracks.

At the big banks, non-performing loans sit near 2%. At the small banks, the Sparkassen and the cooperatives, the corporate book has quietly climbed to 5.16%, up about a third since 2023 and still rising. Not households. Commercial property and small firms. Germany, Austria and Italy carry most of it, right where corporate insolvencies are running hot.

I pulled this live from the ECB's own API, cleaned it, and laid it out as a short deck.

The full dataset, eight tables, copy-as-markdown, is at tigzig.com/ecb-npl-data-tables.

And across the Atlantic...US bank headline is calm too, but the strain sits elsewhere, on the consumer, cards and autos, and in private credit, where losses hit the P&L directly and never show as a bank charge-off. Similar headline, different cracks.

ECB NPL Note - 10-Slide Deck

Browse the slides or download the PDF

tigzig.com, the analyst's tool shed. Built AI-agent-first, point your agent at it and it figures out the rest. Humans welcome.

Full Deck Content (Text Format)

Text below was extracted from the source deck. Chart visuals stay in the PDF and as slide images above the post.

Slide 1 - A calm number, hiding where the stress is

Euro-area banks · non-performing loans · released 19 June 2026.

Euro-area non-performing loans are near a decade low. But split the big banks from the small, and the small banks have pulled ahead.

The small banks have gone from cleaner than the big banks to worse, and the gap is widening.

Source: ECB Supervisory Banking Statistics, via the ECB SDMX API.

Slide 2 - The stress is on the corporate side

Split the small banks' book and only one half is moving.

The consumer book is steady. The corporate book is the engine.

Source: ECB supervisory banking data, via the ECB SDMX API, Q4 2025.

Slide 3 - What is under stress: property and small firms

Two corporate corners carry the stress: commercial real estate and small-business loans.

Commercial real estate and small-business lending: the two corners under the most pressure.

Rates: ECB supervisory data (SDMX API), Q4 2025. Context: ECB SREP 2025; OeNB FSR 51 (Apr 2026).

Slide 4 - In the supervisors' own words

The qualitative read from the supervisors matches the numbers.

Commercial-property issues "continued to weigh on asset quality, particularly in jurisdictions with historically low NPLs such as Germany, Austria, Estonia and Luxembourg." - ECB, Supervisory Review (SREP) 2025

"SME exposures remained a source of concern, as corporate insolvencies... remained elevated... particularly for highly leveraged firms and export-oriented sectors (automotive, chemical, pharmaceutical)." - ECB, Supervisory Review (SREP) 2025

"The loan quality of small and medium-sized enterprises and commercial real estate companies remains strained." - OeNB (Austria's central bank), Financial Stability Report 51, April 2026

Supervisors have acted: tailored letters went to banks, with most measures due by end-2026.

Slide 5 - But keep it in proportion

The small banks are only 15% of euro-area bank assets, so the average hides them.

15% of the system, but this is where the corporate stress is concentrated.

Slide 6 - Where it lives

A few specific systems, not simply the big countries.

Households stay calm in the big systems (Germany 1.6%, Netherlands 0.7%); only small markets like Greece run hot. The euro-area signal is corporate.

Sources: ECB supervisory banking data (SDMX API), Q4 2025; Banca d'Italia FSR No.2 2025.

Slide 7 - The backdrop: more firms failing

Corporate failures have turned up across exactly the three systems showing the bank stress.

+57% Germany: May 2026 corporate insolvencies vs the 2016-19 pre-pandemic May average (IWH early indicator)

6,810 Austria: full-year 2025, +3.4% on 2024 and a fresh high; property-sector failures +35%

+38% Italy: 2025 versus 2024, among the steepest rises in Europe (Allianz Trade)

Failures are rising across all three stress pockets, with property the common thread. A cycle to watch, rather than a system in trouble.

Sources: IWH Insolvenztrend (May 2026); Reuters/Destatis (Dec 2025); KSV1870 (Jan 2026); Allianz Trade (Oct 2025); ECB FSR (May 2026).

Slide 8 - Data and coverage

Where the numbers come from, and the one timing rule that governs the comparisons.

Data source

Extracted via the ECB SDMX REST API (data-api.ecb.europa.eu/service/data/SUP/) on 20 June 2026, and cross-checked against the ECB Supervisory Banking Statistics quarterly publications. The publication links on the Sources page are the human-readable equivalent of the same SDMX records.

Frequency and timing

These supervisory series are quarterly, the highest frequency available. Big-bank (SII) data runs to Q1 2026, released 19 June 2026. Small-bank (LSI) data is published one quarter later by design, so the latest is Q4 2025 (LSI Q1 2026 is due 16 July 2026). Every SII-versus-LSI comparison therefore uses the same quarter, Q4 2025.

Coverage

SII and LSI together are the whole euro-area supervised banking system, about 1,920 banks and EUR 33.8 trillion of assets under the Single Supervisory Mechanism (109 significant banks at about 85% of assets, roughly 1,811 less-significant ones at about 15%). This is the complete sector, not a sample.

A few bank-like activities sit outside it, branches of non-EU banks, standalone investment firms and money-market funds, but they are minor for a loan-book and NPL view.

Segments, country view, and OeNB

CRE and SME NPL ratios are published at the big-bank level; the small-bank split is not published euro-area-wide, so Austria (OeNB, the Oesterreichische Nationalbank) is used as a concrete small-bank example. Country book size uses published LSI total assets; euro NPL volumes are not estimated.

Not just an API call, the full dataset is published. Every figure here is downloaded, cleaned and organised into eight tables (seven from the ECB API, plus the IWH insolvency series), each copyable as markdown in one click: tigzig.com/ecb-npl-data-tables.

Slide 9 - Definitions

What the numbers mean, in the ECB's own terms.

Non-performing loan (NPL)

A loan is non-performing when the borrower is "unlikely to repay", or when "more than 90 days have passed" without payment. It is a stock measure, the outstanding balance of non-performing loans as a share of gross loans (excluding central-bank cash), not a charge-off or loss rate. Comparable to a gross non-performing-asset ratio. (ECB and EBA definition.)

Big banks (significant institutions, SII)

The largest banking groups, supervised directly by the ECB, about 85% of euro-area bank assets. In the composition we combine the published categories: global systemically important banks (G-SIBs), universal and diversified lenders, retail and consumer lenders, and other significant institutions.

Small banks (less significant institutions, LSI)

Smaller banks supervised by national authorities under ECB oversight, about 15% of euro-area bank assets. In several countries these are savings and cooperative banks.

Slide 10 - Sources

ECB and national primary data; every figure cross-checked to the published source.

ECB Supervisory Banking Statistics

The bank-size and sector NPL data, the spine of this note. Pulled via the ECB SDMX API; Q1 2026 release for the big banks (19 June 2026), Q4 2025 for the small banks. bankingsupervision.europa.eu · data.ecb.europa.eu

ECB SREP 2025 · OeNB Financial Stability Report 51 · ECB FSR May 2026

CRE stress "particularly in Germany, Austria, Estonia, Luxembourg"; SME "a source of concern" (ECB SREP, Nov 2025). Austria small-bank CRE 8.3% / SME 6.3% and "strained" (OeNB, Apr 2026). Insolvencies "risen sharply" (ECB FSR, May 2026).

Corporate insolvencies

Germany: IWH monthly early indicator 57% above the pre-pandemic norm, May 2026 (1,518 cases); full-year 2025 ~23,900 (+8.3%), highest since 2014. Austria 6,810 (+3.4%), property failures +35% (Jan 2026). Italy ~+38%, among Europe's steepest (Oct 2025). IWH Insolvenztrend · Reuters/Destatis · KSV1870 · Allianz Trade.

Banca d'Italia Financial Stability Report No.2 2025

Italian small banks showed "overall resilience" in stress tests (Nov 2025). bancaditalia.it